Aesthetic Medicine Market Overview & Analysis

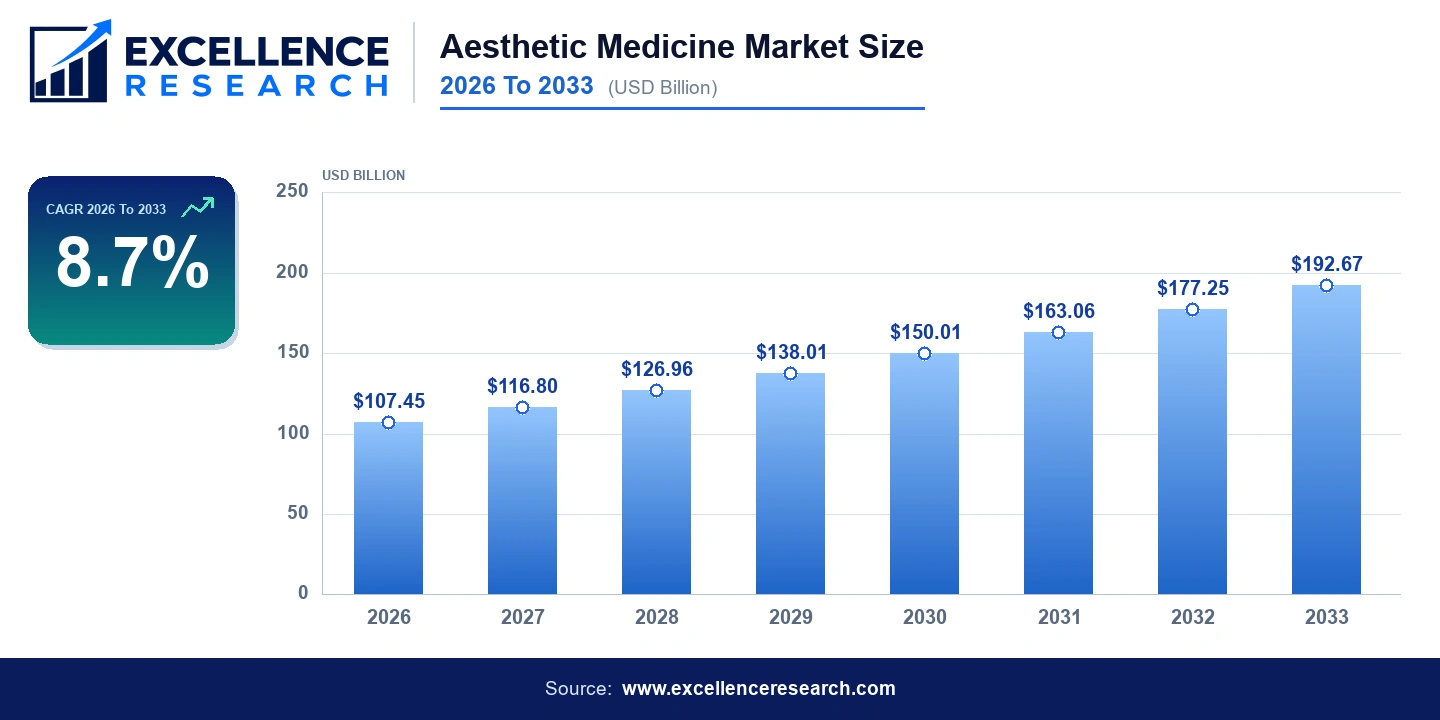

The global aesthetic medicine market is valued at USD 107.45 billion in 2026 and is projected to reach USD 192.67 billion by 2033, advancing at a compound annual growth rate of 8.7% over the forecast period. This robust expansion reflects accelerating consumer demand for both surgical and non-surgical appearance enhancement procedures across mature and emerging economies alike. Rising disposable incomes, growing social media influence on beauty standards, and the increasing normalization of cosmetic treatments among millennial and Generation Z demographics are collectively fueling sustained market momentum. The market spans more than 45 countries, with significant growth corridors identified across North America, Europe, and the Asia-Pacific region, where regulatory modernization and expanding clinic infrastructure are enabling broader patient access.

Key Report Takeaways

- By Procedure: Non-invasive procedures held the largest revenue share in 2026, driven by strong demand for botulinum toxin injections and dermal fillers, while non-invasive procedures also represent the fastest-growing category, projected to outpace invasive surgical alternatives throughout the forecast period due to shorter recovery times and lower cost barriers.

- By End Use: Clinics and aesthetic centers held the dominant share of patient visits and revenue in 2026, capturing approximately 48% of global end-use demand, while medspas are the fastest-growing end-use segment as operators expand hybrid medical-wellness service offerings in suburban and secondary urban markets.

Market Drivers

The primary catalyst accelerating aesthetic medicine adoption is the democratization of minimally invasive procedures. Treatments such as hyaluronic acid-based dermal fillers, botulinum toxin type A formulations like AbbVie's Botox and Galderma's Dysport, and energy-based body contouring technologies have become increasingly accessible to middle-income consumers. The average cost of a neuromodulator treatment in the United States declined by approximately 12% between 2019 and 2024 as competitive pricing from biosimilar entrants and expanded provider networks placed downward pressure on procedure costs. This affordability trend is drawing a significantly broader patient base, with the American Society of Plastic Surgeons reporting that individuals aged 20 to 39 now account for more than 30% of all minimally invasive cosmetic procedure volumes in North America.

Technological innovation is a second major driver reshaping competitive dynamics and expanding the addressable market. Platforms integrating radiofrequency microneedling, high-intensity focused ultrasound, and cryolipolysis are enabling practitioners to deliver measurable clinical outcomes with minimal downtime. Cynosure's PicoSure platform and Lumenis Be Ltd.'s LEGEND PRO system exemplify how multi-application energy devices are allowing smaller aesthetic clinics to offer a wider procedural menu without proportional increases in capital expenditure. Additionally, advances in artificial intelligence-assisted treatment planning and augmented reality consultation tools are reducing patient hesitancy and shortening the decision cycle from inquiry to booking, directly boosting procedure volumes across established and emerging markets.

Segment Analysis

By Procedure: Non-invasive procedures constitute the dominant revenue segment within the aesthetic medicine market, accounting for an estimated 61% of total market value in 2026. This segment encompasses neuromodulators, soft tissue fillers, laser and light-based skin treatments, chemical peels, and body contouring technologies. The global botulinum toxin market alone exceeded USD 7 billion in 2025, with AbbVie and Galderma controlling a combined share exceeding 55% of the branded neuromodulator segment. Invasive procedures, including rhinoplasty, blepharoplasty, liposuction, and breast augmentation, retain a stable patient base driven by individuals seeking permanent or long-duration structural changes. Johnson and Johnson's surgical aesthetics portfolio, operating through its MedTech segment, and Hologic's breast health technologies contribute meaningfully to the invasive procedure revenue stream. Invasive procedures carry higher average revenue per case, with a primary rhinoplasty averaging USD 5,400 in the United States in 2024 according to the American Society of Plastic Surgeons, providing a pricing counterbalance to the volume advantage held by non-invasive treatments.

By End Use: Clinics and aesthetic centers represent the largest end-use segment, benefiting from physician-owned private practice models that offer specialized expertise and a curated procedural environment preferred by patients seeking higher-acuity treatments. Medspas are registering the highest growth rate within the end-use segment, with the International Spa Association estimating more than 8,100 medspa locations operating in the United States alone as of 2024, a figure that has grown at approximately 12% annually since 2021. Medspas attract a recurring client base through membership models, bundled treatment packages, and retail skincare integration. Hospitals maintain a steady share of the invasive procedure volume, particularly for reconstructive and post-oncological aesthetic interventions, with academic medical centers and specialty cosmetic surgery hospitals serving as training centers for emerging procedural techniques.

Regional Analysis

North America remains the largest regional market for aesthetic medicine, accounting for approximately 38% of global revenues in 2026. The United States anchors this position, supported by a mature regulatory framework administered by the U.S. Food and Drug Administration, high per-capita healthcare spending, and an entrenched culture of aesthetic self-improvement. In 2023, the American Society of Plastic Surgeons reported more than 26.2 million cosmetic procedures performed in the United States alone. The region is home to the headquarters and primary research and development operations of key players including AbbVie Inc., Cynosure, Solta Medical, Candela Medical, and Hologic, Inc., reinforcing its position as an innovation hub that sets procedural trends subsequently adopted globally.

Europe holds the second-largest regional share, estimated at approximately 27% of global market value in 2026. Germany, France, the United Kingdom, Italy, and Spain constitute the five largest national markets within the region. Galderma, headquartered in Zug, Switzerland, commands particularly strong market penetration across European dermatology and aesthetic clinic networks. The European market is characterized by rigorous regulatory oversight under the Medical Device Regulation framework, which came into full effect in 2021 and has elevated product approval standards, concentrating market share among well-capitalized manufacturers capable of meeting enhanced clinical evidence requirements. Medical tourism corridors, particularly into Turkey, Czech Republic, and Hungary, are drawing patients from Western Europe seeking lower-cost access to both invasive and non-invasive procedures.

Asia-Pacific is the fastest-growing regional market, projected to sustain a CAGR exceeding 11% through 2033, outpacing the global average by a meaningful margin. South Korea maintains its status as the regional epicenter of aesthetic innovation, with Seoul's Gangnam district hosting more than 500 cosmetic surgery clinics and the country exporting its surgical expertise and beauty standards through the Korean Wave cultural influence. China represents the largest volume opportunity within the region, with the National Medical Products Administration approving a growing roster of domestic and international aesthetic devices and injectables. Japan, India, and Australia are also recording accelerating procedure volumes as awareness campaigns by market participants including Alma Lasers and Lumenis Be Ltd. expand practitioner networks and consumer familiarity with energy-based treatment modalities.

Competitive Landscape

The aesthetic medicine market is moderately consolidated at the product manufacturer level, with a defined group of multinational corporations competing for share across injectable biologics, energy-based devices, and consumable supplies. AbbVie Inc. occupies the leading position globally, driven by the Botox Cosmetic and Juvederm portfolio, which together generate more than USD 5 billion in annual aesthetics revenue and underpin the company's strategic priority of expanding its Medical Aesthetics business unit. Galderma, following its initial public offering on the SIX Swiss Exchange in March 2024, operates with a pure-play aesthetics and dermatology focus, anchoring its competitive position through the Restylane filler collection, Sculptra, Dysport, and the Cetaphil skincare line. In the energy-based device segment, Cynosure, Alma Lasers, Lumenis Be Ltd., Solta Medical, and Candela Medical compete on the basis of platform versatility, clinical outcome data, and practitioner training programs. Johnson and Johnson's MedTech aesthetics segment and Hologic's breast health and body contouring business add scale-advantaged competition within surgical and device categories. Dentsply Sirona, while primarily a dental technology company, participates in adjacent aesthetic markets through oral and maxillofacial aesthetics. Strategic priorities across the competitive landscape include geographic expansion into Asia-Pacific, product portfolio broadening through acquisition, and investment in subscription-based service models to deepen customer retention within clinic and medspa networks.

Recent Developments

- 2024: Galderma completed its initial public offering on the SIX Swiss Exchange in March 2024, raising approximately CHF 2.3 billion in the largest European healthcare IPO of the year, with the proceeds designated to accelerate product development and geographic expansion across Asia-Pacific and Latin American markets.

- 2024: AbbVie received U.S. FDA approval for Botox Cosmetic in a new concentration formulation targeting moderate-to-severe forehead lines, extending the labeled indications of the product and opening an incremental patient population estimated at 4 million eligible adults in the United States.

- 2023: Cynosure launched the Icon Max system, an upgraded iteration of its flagship intense pulsed light and fractional laser platform, incorporating machine learning-assisted fluence optimization to reduce operator variability and improve patient outcome consistency across its installed base of more than 12,000 clinical sites worldwide.

- 2023: Alma Lasers finalized the acquisition of Syneron-Candela's non-core product lines in select European territories, expanding its radiofrequency and light-based device portfolio and adding approximately 300 active clinic accounts to its European distribution network as part of a broader strategy to consolidate its position among the top three energy-based device providers in the region.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Aesthetic Medicine Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $107.45B |

| Market Size (2033) | $192.67B |

| CAGR | 8.700% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Procedure, And End Use |

| Companies Covered | AbbVie Inc., Galderma, Alma Lasers, Cynosure, Johnson & Johnson Private Limited, Lumenis Be Ltd., Solta Medical, Candela Medical, Hologic, Inc., Dentsply Sirona |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Frequently Asked Questions — Aesthetic Medicine Market

You May Also Like

Specialist in Healthcare market intelligence.

Schedule Free Analyst Call