Remote Neurological Monitoring Market Overview & Analysis

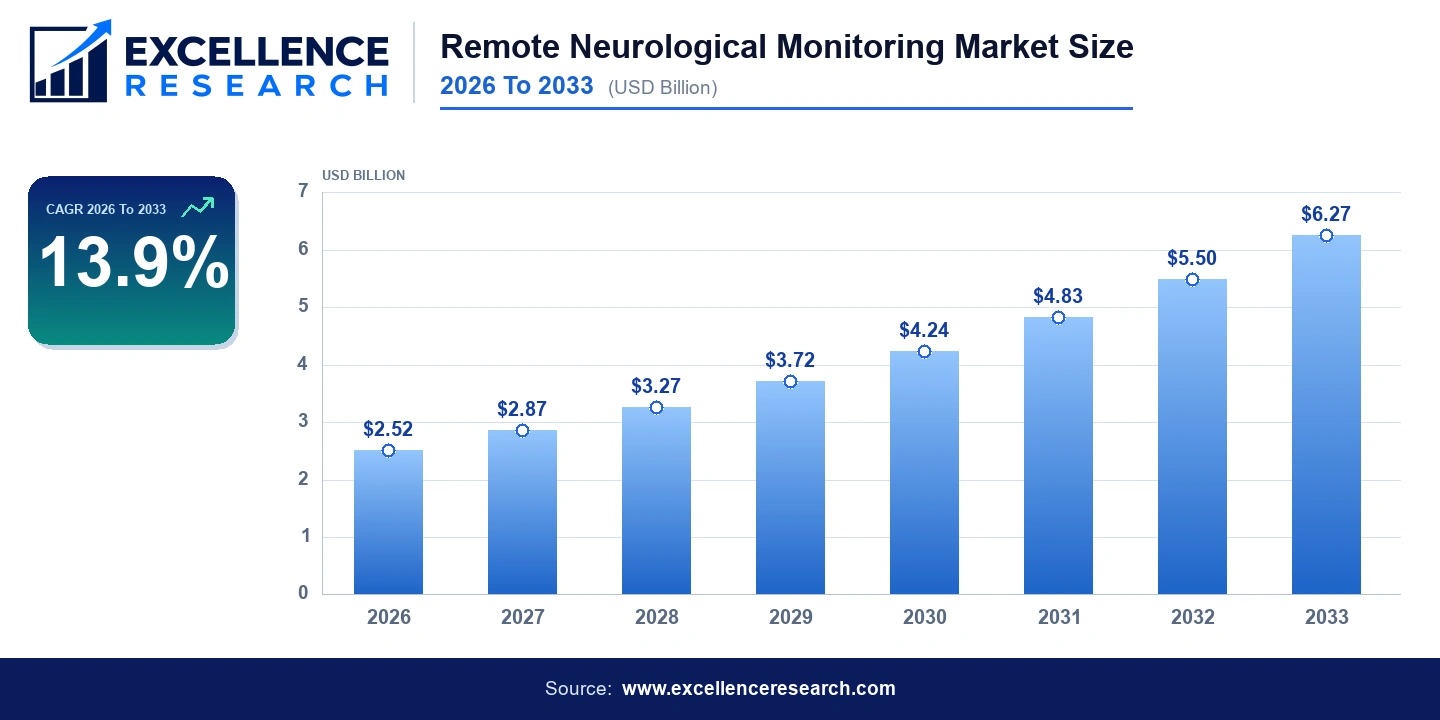

Remote neurological monitoring sits at the intersection of neuroscience, digital health infrastructure, and chronic disease management, representing one of the most technically demanding segments within the broader connected healthcare space. The market encompasses a wide array of technologies including ambulatory EEG systems, implantable neurostimulators with telemetry capability, AI-driven seizure detection platforms, wearable EEG headsets, and cloud-based clinical data management software. Its strategic importance extends well beyond convenience. With neurological disorders affecting an estimated 3.4 billion people globally according to a 2024 Lancet Neurology analysis, the gap between demand for specialist neurological assessment and the supply of trained neurologists, approximately 0.1 neurologists per 100,000 population in low-income countries, has made remote monitoring not a luxury but a structural necessity. Payers, health systems, and pharmaceutical sponsors are all recalibrating their investment priorities accordingly. The global remote neurological monitoring market was valued at USD 2.52 billion in the base year 2026 and is projected to reach USD 6.27 billion by 2033, expanding at a compound annual growth rate of 13.9% over the forecast period. This trajectory is notably steeper than the 8.4% CAGR recorded across the broader medical devices sector during 2021 to 2025, reflecting specific tailwinds unique to neurological applications. The market nearly doubled in absolute dollar terms from 2021 to 2025, driven by accelerated telehealth adoption during and after the COVID-19 pandemic, and the momentum has not unwound. Total incremental revenue generated across the forecast window is expected to exceed USD 3.75 billion, with the highest single-year absolute gains anticipated in 2031 and 2032 as AI-integrated diagnostic platforms achieve mainstream clinical acceptance in Western European and Asia Pacific health systems. Several converging forces are accelerating adoption across the care continuum. The prevalence of epilepsy alone, affecting roughly 50 million people worldwide per the World Health Organization, creates a persistent and quantifiable patient pool for continuous remote EEG monitoring. NeuroPace's RNS System, the only closed-loop responsive neurostimulation device cleared by the FDA for drug-resistant focal epilepsy, has accumulated over 4,000 implanted patients in the United States and generates actionable long-term EEG data streams that clinicians access remotely via the NeuroPace Patient Data Management System. Medtronic has positioned its Percept PC deep brain stimulator, equipped with BrainSense Technology, as a remote data capture tool for Parkinson's disease management, with sensing capabilities that allow neurologists to review LFP brain signal data between in-person visits. These device-level innovations are being layered with software intelligence. BioSerenity, the French medtech company, markets the Neuronaute wearable EEG system specifically designed for remote seizure monitoring in ambulatory and home settings, and its partnership with Biogen announced in 2023 underscored how pharmaceutical sponsors are embedding remote neurological monitoring into late-phase clinical trial protocols. The rising use of real-world evidence in regulatory submissions is a genuine structural demand driver that many generalist analyses underweight. Geographically, North America commands the largest share of the global market, accounting for an estimated 38% of total revenue in 2026, supported by favorable reimbursement for remote patient monitoring under CMS CPT codes 99453, 99454, and 99457, and by high per-capita neurologist density in states such as Massachusetts, California, and New York. Europe holds approximately 27% of global share, with Germany, France, and the United Kingdom collectively representing over two thirds of regional revenue. Germany's digitale Gesundheitsanwendungen framework, which enables reimbursement of digital health applications including some neurology-specific tools through the statutory health insurance system, has given the European market a regulatory catalyst absent in many other regions. Asia Pacific is the fastest-growing region, expected to record a CAGR of approximately 16.2% through 2033, driven by China's aggressive hospital digitization agenda under the 14th Five-Year Plan, India's expanding telemedicine infrastructure post the Telemedicine Practice Guidelines 2020, and Japan's aging population where dementia prevalence is projected to reach 7 million by 2025. Latin America and Middle East and Africa collectively represent under 10% of current market value but offer disproportionate long-run upside given low baseline penetration. The competitive environment is bifurcated between large diversified medtech and healthtech incumbents with established clinical relationships and smaller specialized companies competing on technological differentiation. Medtronic and Philips represent the scale players. Philips' EncoreAnywhere sleep and neurological data management platform and its integration with the IntelliVue patient monitoring ecosystem give it strong positioning in hospital-based and post-acute settings. GE HealthCare, following its spin-off from General Electric in January 2023, has accelerated its neurology software investments, with its CARESCAPE monitoring platform seeing growing deployment in neurological ICU environments. Masimo, better known for its pulse oximetry dominance, has been extending its Masimo W1 and Root platforms into neurological parameter monitoring, including cerebral oximetry via its SedLine Brain Function Monitor cleared for OR and ICU use. Natus Medical, now operating under Integra LifeSciences after its 2017 acquisition, remains one of the most widely installed EEG hardware providers globally. Compumedics, the Australian company, commands a niche premium in polysomnography and quantitative EEG research applications, with its Grael and Neuvo systems found in academic medical centers across North America and Europe. The critical observation here is that no single vendor controls more than 12 to 14% of the total addressable market, making this a fragmented arena where M&A activity will be a defining feature of the competitive story through 2033. The market faces real constraints that growth narratives tend to obscure. Data privacy regulations present meaningful friction. Neurological data, particularly continuous EEG or brain signal data from implanted devices, is classified under GDPR Article 9 as sensitive health data in Europe, and equivalent state-level protections under California's CMIA and emerging laws in states like Colorado and Texas create a compliance burden that smaller vendors struggle to absorb. Reimbursement remains inconsistent outside of the United States. In most Asia Pacific markets outside Japan and Australia, remote neurological monitoring services attract limited or no specific payer coverage, forcing providers to embed costs within general consultation fees or rely on out-of-pocket payment. Connectivity infrastructure gaps in rural Sub-Saharan Africa and parts of Southeast Asia limit the practical deployment of high-bandwidth continuous monitoring systems. One frequently overlooked restraint is clinician workflow integration. Hospital neurologists in high-volume centers report alert fatigue from AI-generated notifications in early-generation remote monitoring platforms, a problem that has slowed adoption even in well-resourced systems, and one that vendors have not fully resolved. The most significant emerging opportunities lie in three areas. AI-driven biomarker discovery is opening new commercial territory. Platforms capable of detecting subclinical seizure signatures, early Alzheimer's biomarkers via EEG spectral analysis, or psychiatric state changes via continuous monitoring are advancing from research settings toward commercial viability. Companies such as Beacon Biosignals, acquired by Nuvation Bio in 2022, and Neurolutions are developing proprietary signal processing algorithms that could redefine diagnostic value in neurological monitoring. The integration of remote neurological monitoring into Phase II and III clinical trials represents a second high-value opportunity, particularly as the FDA's Real World Evidence Program and EMA's adaptive licensing pathways increase appetite for continuous remote data collection as a complement to traditional clinical endpoints. Home care end-users represent the third frontier. With an estimated 60% of epilepsy patients in high-income countries having uncontrolled seizures and lacking hospital admission, home-based automated EEG monitoring with cloud-integrated neurologist review is both clinically necessary and commercially scalable. The 2026 to 2033 forecast period will test which companies can navigate regulatory complexity, reimbursement heterogeneity, and clinical workflow demands well enough to capture that growth.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Remote Neurological Monitoring Market Size, Share, Trends & Forecast 2026 To 2033 |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $2.52B |

| Market Size (2033) | $6.27B |

| CAGR | 13.900% |

| Regions Covered | Global (60+ countries) |

| Segments Covered | Product Type, Voltage Rating, Application, And Region |

| Companies Covered | Medtronic, NeuroPace, Natus Medical, Compumedics, Masimo, Philips, GE HealthCare, BioSerenity, Ceribell, Empatica, Brain Scientific, Wearable Sensing and others |

Segmentation Covered

Key Companies Profiled (15)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Remote Neurological Monitoring Market

You May Also Like

Specialist in Healthcare & Life Sciences market intelligence.

Schedule Free Analyst Call