Anti-Obesity Drugs Market Overview & Analysis

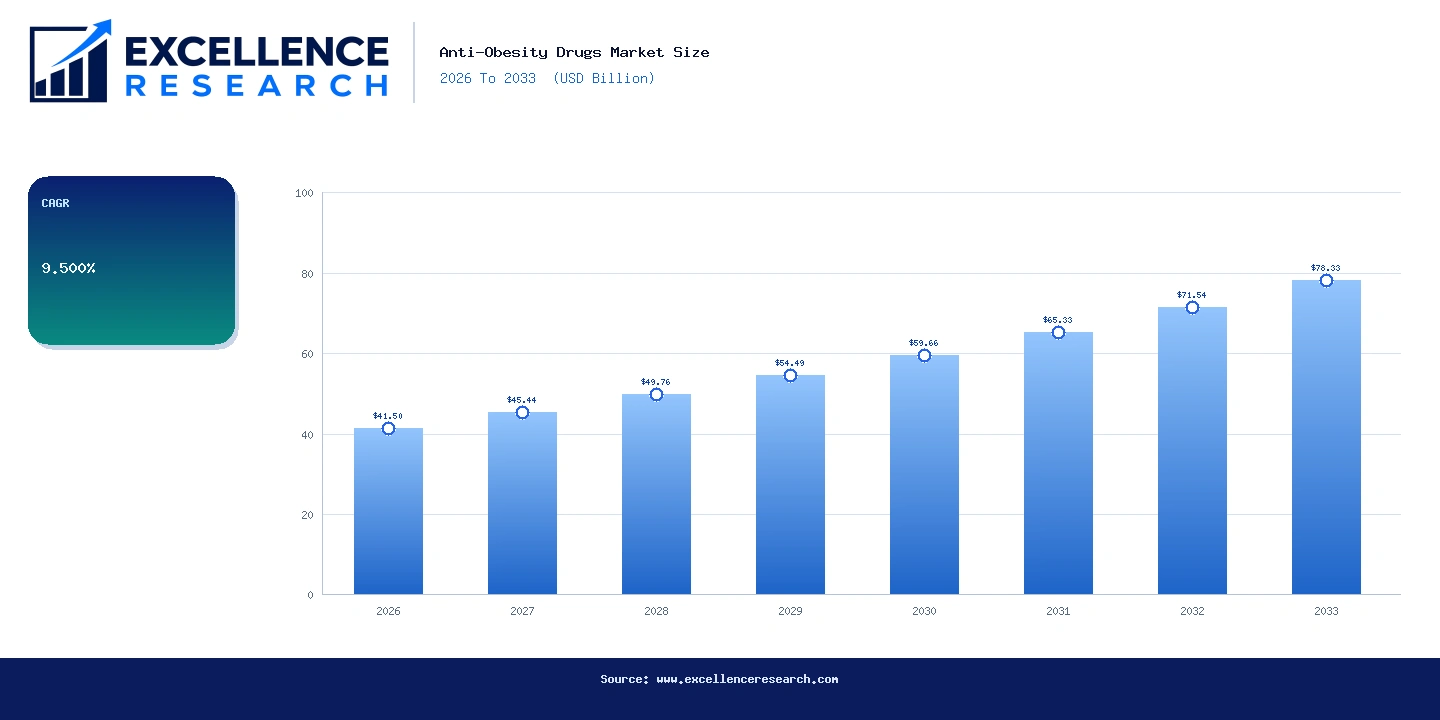

The global anti-obesity drugs market was valued at USD 41.5 billion in 2026 and is projected to reach USD 78.33 billion by 2033, expanding at a compound annual growth rate of 9.5% over the 2026 to 2033 forecast period. This trajectory reflects a structural shift in how healthcare systems worldwide are treating obesity, moving away from purely behavioral and surgical interventions toward pharmacological management backed by robust clinical evidence. Historical data from 2021 to 2025 shows accelerating uptake, driven largely by the commercial success of glucagon-like peptide-1 receptor agonists, most visibly Novo Nordisk's semaglutide franchise under the Wegovy and Ozempic brand names. The market now spans more than 55 countries, with payer coverage expansions, growing physician familiarity, and a deepening pipeline collectively sustaining the high single-digit growth rate expected through the decade.

Key Report Takeaways

- By drug class: GLP-1 receptor agonists held the largest revenue share in 2026, exceeding 58% of total market value, while dual GIP/GLP-1 agonists represent the fastest-growing class at an estimated 18.2% CAGR through 2033.

- By route of administration: injectable formulations dominated with approximately 72% share in 2026; oral anti-obesity agents are the fastest-growing sub-segment as pill-based semaglutide and orforglipron advance commercially.

- By distribution channel: hospital pharmacies held the leading position in 2026, while specialty and retail pharmacies are gaining share rapidly as outpatient prescriptions normalize globally.

- By end user: adults aged 35 to 64 years constitute the core patient population and the highest revenue segment; the adolescent and young adult cohort is the fastest-growing end-user group, supported by expanded FDA and EMA label indications.

- By region: North America commanded the largest regional share at approximately 48% in 2026, while the Asia Pacific region is forecast to record the highest CAGR of 13.1% through 2033, led by China, Japan, and South Korea.

Market Drivers

The primary force behind market expansion is the sheer scale of the obesity epidemic. The World Obesity Federation estimated in 2023 that more than one billion people globally live with obesity, a figure projected to exceed 1.9 billion by 2035. This creates an enormous addressable patient pool that current drug supply has not yet fully served. Weight-related comorbidities including type 2 diabetes, hypertension, non-alcoholic steatohepatitis, and obstructive sleep apnea are generating parallel clinical demand, with physicians increasingly prescribing anti-obesity medications as a multi-indication tool rather than a single-purpose weight loss agent. The SELECT cardiovascular outcomes trial, which demonstrated a 20% reduction in major adverse cardiovascular events with semaglutide 2.4 mg in non-diabetic patients, was a turning point. That data has opened the door to cardiovascular risk reduction as a standalone reimbursable indication, materially widening the prescribing universe beyond endocrinologists to cardiologists and primary care physicians.

Payer coverage remains one of the most consequential variables in the commercial trajectory. In the United States, the Centers for Medicare and Medicaid Services has been under sustained legislative pressure to include anti-obesity medications in Part D formularies following the Treat and Reduce Obesity Act. Several large commercial insurers, including CVS Aetna and Cigna, have expanded or tiered coverage for branded GLP-1 therapies, and employer self-funded health plans are increasingly offering weight management benefits to attract and retain talent. Outside the United States, the United Kingdom's National Health Service authorized a two-year Wegovy rollout through specialist weight management services in 2023, and Germany's statutory insurers are piloting structured reimbursement pathways. These policy shifts, occurring across multiple major healthcare markets simultaneously, compound the organic patient demand already generated by media visibility and direct-to-consumer awareness campaigns.

Segment Analysis

By Drug Class: GLP-1 receptor agonists anchor the market. Semaglutide, sold as Wegovy for chronic weight management and Ozempic for type 2 diabetes, generated combined revenue exceeding USD 21 billion globally in 2024 for Novo Nordisk. Liraglutide, marketed as Saxenda, remains commercially relevant but is experiencing volume erosion as semaglutide's superior efficacy profile captures new prescriptions. The most consequential emerging class is the dual glucose-dependent insulinotropic polypeptide and GLP-1 receptor agonist category, where Eli Lilly's tirzepatide, branded as Zepbound for obesity, posted U.S. sales of approximately USD 4.9 billion in 2024 alone, demonstrating an adoption velocity that has surprised even the most optimistic forecasts. Oral small molecule candidates and amylin analogs constitute an early-stage but high-potential segment that could redefine accessibility economics before 2030.

By Route of Administration: Subcutaneous injectables currently define the market's clinical and commercial mainstream, with weekly dosing regimens improving patient adherence compared to daily injections used with older formulations like liraglutide. The shift toward orally administered options is not merely a patient preference story. It carries genuine access implications for markets with cold-chain distribution constraints across Southeast Asia, Sub-Saharan Africa, and rural Latin America. Pfizer's danuglipron and Eli Lilly's orforglipron are in late-stage development, and success in Phase 3 trials would unlock an entirely new commercial channel. This sub-segment warrants close attention given its disproportionate long-term growth potential relative to its current revenue base.

By Distribution Channel: Hospital-based dispensing dominates in markets with centralized healthcare delivery, particularly across continental Europe and East Asia. In the United States, the shift to retail and specialty pharmacy has been pronounced, with chains such as CVS and Walgreens, as well as telehealth-adjacent platforms like Hims and Hers and Ro, playing a measurable role in expanding patient access. Compounding pharmacies occupied a significant and legally contentious position during the 2023 to 2024 semaglutide shortage, a dynamic that has drawn intense regulatory scrutiny from the FDA and is expected to normalize as branded supply constraints ease.

Regional Analysis

North America retained approximately 48% of global market revenue in 2026. The United States alone accounted for the vast majority of that share, driven by high drug pricing, broad commercial insurance penetration relative to other markets, and a population where adult obesity prevalence exceeds 42% according to the Centers for Disease Control and Prevention. Canada is a smaller but growing market as provincial drug plans expand coverage criteria.

Europe represented approximately 24% of global revenue in 2026. The region's growth is tempered by reference pricing mechanisms and health technology assessment bodies such as NICE in the United Kingdom, IQWIG in Germany, and HAS in France, which apply cost-effectiveness thresholds that have constrained reimbursement breadth. Nevertheless, the absolute patient volumes in Germany, France, Italy, and the United Kingdom are substantial, and ongoing HTA recalibrations are expected to improve market access between 2027 and 2030.

Asia Pacific is forecast to post the fastest regional CAGR at 13.1% through 2033. China's National Medical Products Administration approved a domestic manufacturing pathway for semaglutide, and local pharmaceutical companies including Hengrui Medicine are developing proprietary GLP-1 candidates. Japan's aging but increasingly weight-burdened population, combined with government support for metabolic disease management, is creating a structured demand base. South Korea and Australia are smaller but increasingly relevant markets with favorable regulatory environments.

Latin America and the Middle East and Africa collectively accounted for roughly 8% of market value in 2026. Brazil leads Latin American uptake given its large private health insurance sector and high urban obesity rates. Gulf Cooperation Council states, particularly Saudi Arabia and the UAE, are active early-adopter markets given high obesity prevalence and substantial out-of-pocket healthcare spending capacity among affluent urban populations.

Competitive Landscape

The anti-obesity drugs market is currently a duopoly at the branded level, with Novo Nordisk and Eli Lilly controlling the overwhelming majority of commercially available weight-loss prescription revenue. Novo Nordisk's semaglutide franchise represents the incumbent position, backed by multiple approved indications and global manufacturing scale built over several years. Eli Lilly's tirzepatide has mounted a rapid competitive challenge, with clinical data showing average weight reductions of up to 22.5% in the SURMOUNT-1 trial, exceeding semaglutide's published efficacy benchmarks. This competitive dynamic is driving aggressive pricing negotiations, supply investment, and pipeline acceleration from both companies. Roche's acquisition of Carmot Therapeutics in late 2023 for approximately USD 2.7 billion signaled the return of a major pharmaceutical conglomerate to the obesity space after decades of absence. AstraZeneca, Pfizer, and Amgen are each advancing candidates at various clinical stages, and the entry of even one or two additional commercially successful agents before 2033 could meaningfully reshape market concentration. The competitive axis is shifting from efficacy differentiation toward total value propositions encompassing cardiovascular outcomes, renal protection data, oral bioavailability, and manufacturing cost economics.

Recent Developments

- 2025: Eli Lilly received FDA approval for tirzepatide (Zepbound) as a treatment for moderate-to-severe obstructive sleep apnea in adults with obesity, marking the first pharmacological approval for this combined indication and substantially broadening the eligible prescribing population.

- 2024: Novo Nordisk initiated construction of a dedicated semaglutide manufacturing facility in Clayton, North Carolina, representing a capital commitment of approximately USD 4.1 billion, with production capacity expected to come online in phases through 2027 to address persistent global supply shortfalls.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Anti-Obesity Drugs Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $41.50B |

| Market Size (2033) | $78.33B |

| CAGR | 9.500% |

| Regions Covered | Global |

| Segments Covered | Drug Class, Patient Indication, Distribution Channel, Payer Type, And Region |

| Companies Covered | Novo Nordisk, Eli Lilly and Company, Roche, AstraZeneca, Pfizer, Amgen, Boehringer Ingelheim, Viking Therapeutics, Structure Therapeutics, Rhythm Biosciences |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Frequently Asked Questions — Anti-Obesity Drugs Market

You May Also Like

Specialist in Healthcare & Life Sciences market intelligence.

Schedule Free Analyst Call