AI Companion App Market Overview & Analysis

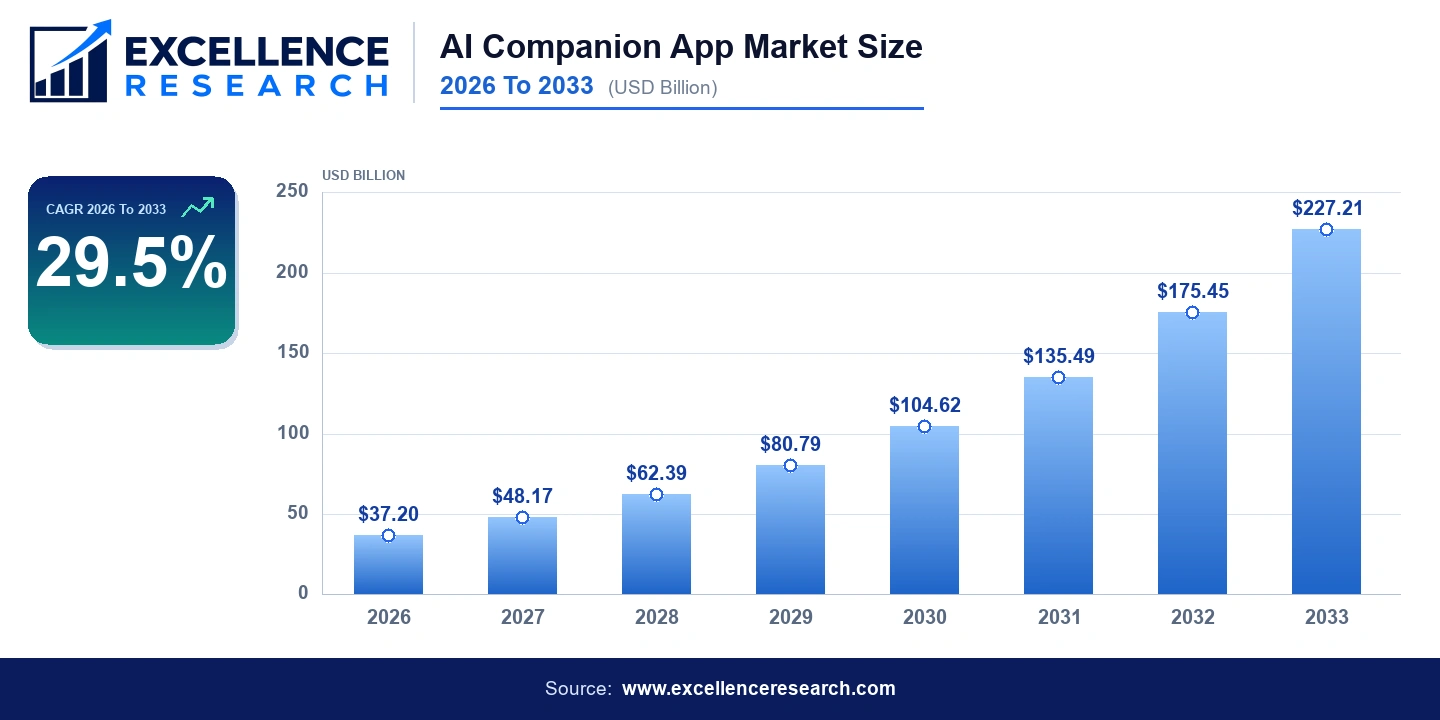

The global AI companion app market was valued at USD 37.2 billion in 2026 and is projected to reach USD 227.21 billion by 2033, at a CAGR of 29.5% during the forecast period (2026 to 2033). The category sits at the intersection of behavioral psychology, large language model deployment, and consumer subscription economics. Its strategic importance has grown considerably as mental health infrastructure globally fails to keep pace with demand, and as a generation of consumers raised on persistent digital interaction begins seeking ambient social connection through software.

The market has effectively doubled in addressable scale relative to where it stood in 2021, when early products like Replika were still largely niche curiosities. The sharpest inflection is expected between 2028 and 2031 as multimodal interaction capabilities including voice, avatar, and contextual memory reach mass-market readiness across mid-range devices.

Key Report Takeaways

- By use case, Emotional Support and Loneliness Mitigation held the largest share in 2025; Mental Wellness is the fastest-growing use case at 31.2% CAGR through 2033.

- By AI technology, Large Language Model-based companions accounted for 62.4% of the AI companion app market share in 2025; Multimodal AI (voice and avatar) is advancing at 34.8% CAGR through 2033.

- By deployment, Mobile Applications dominated with 71.3% revenue share in 2025; Wearable Integration is forecast to post a 38.5% CAGR between 2026 and 2033.

- By end user, General Consumers captured 58.2% of the market in 2025; Enterprise and B2B2C wellness programs represent the fastest-expanding segment at 32.6% CAGR.

- By region, North America led with 34.0% revenue share in 2025, while Asia Pacific is on track for a 32.1% CAGR through 2033.

Market Drivers

The loneliness epidemic documented in over 40 peer-reviewed studies since 2020 has translated into measurable consumer willingness to pay for digital companionship. In the United States alone, the Surgeon General's 2023 advisory on social isolation quantified the health cost of loneliness as equivalent to smoking 15 cigarettes per day, lending a quasi-clinical justification to products that might otherwise face cultural skepticism.

Rapid advances in large language models have fundamentally changed companion quality. Luka Inc.'s Replika reported over 30 million registered users by late 2024, demonstrating that retention is achievable when products combine emotional continuity with regular feature updates. Character.AI recorded over 20 million monthly active users within two years of launch, driven largely by younger demographics using the platform for roleplay, creative writing, and para-social interaction.

Snap Inc.'s integration of My AI into Snapchat, reaching an installed base of over 750 million users, showed that companion features embedded within existing social infrastructure can normalize the behavior at scale without requiring standalone app adoption. The B2B2C model, where employers license companion wellness tools as employee benefits, is already generating early revenue for companies like Wysa and Woebot Health.

Segment Analysis

By Use Case: Emotional support and loneliness mitigation leads the market because it addresses the most immediate and measurable consumer pain point. Mental wellness is the fastest-growing use case as health systems pilot AI companion tools as cognitive behavioral therapy supplements, targeting the estimated 450 million people globally who cannot access timely mental health care. Enterprise and B2B2C adoption is growing rapidly as employers seek subscription wellness tools that reduce absenteeism and mental health claims.

By AI Technology: Large language model-based companions dominate because they deliver the most natural and emotionally responsive conversation quality at scale. Multimodal AI combining text, voice, and avatar is the fastest-growing technology segment, driven by consumer preference for richer interaction modalities. Apple's rumored health-oriented features in future Apple Watch iterations and Samsung's Galaxy Ring biometric platform could provide companion apps with real-time physiological data to calibrate emotional responsiveness.

By Deployment: Mobile applications lead because smartphones are the primary access point for companion interactions. Wearable device integration is the fastest-growing deployment mode as persistent, ambient computing enables always-on companion presence. Smart home device embedding is gaining traction through partnerships with Amazon Alexa and Google Home ecosystems.

By End User: General consumers dominate by volume, but enterprise and B2B2C segments are growing fastest as corporate wellness programs seek AI-based mental health solutions that can scale across large employee bases without requiring human therapist hours. Elderly and socially isolated users represent an underserved but high-value segment with strong retention characteristics.

Regional Analysis

North America maintained 34.0% revenue share in 2025, anchored by high smartphone penetration, early-adopter consumer culture, and a relatively permissive regulatory environment for AI-generated emotional content. Federal interest in mental health parity and employer wellness mandates further support institutional adoption of companion platforms.

Asia Pacific is the fastest-growing territory at 32.1% CAGR through 2033. China's Xiaoice, originally incubated inside Microsoft and subsequently spun off, has accumulated over 660 million users across Japan, Indonesia, and China, demonstrating that state-adjacent AI companion ecosystems can scale at speeds Western entrants cannot easily replicate. Japan's longstanding cultural acceptance of virtual relationships, evidenced by the commercial success of Gatebox's virtual home assistant, accelerates adoption curves that in Western markets require years of normalization.

Europe trails due to stricter data governance under GDPR and ongoing national regulatory consultations regarding AI companionship for minors. However, digital mental health funding from national health systems in Germany, France, and the UK is creating new procurement channels for clinically validated companion tools. Latin America and Middle East and Africa represent emerging opportunity as smartphone penetration rises and mental health stigma gradually decreases across younger demographics.

Competitive Landscape

The competitive structure of this market is fragmented at the product layer but consolidating at the infrastructure layer. Replika remains the most recognized standalone companion brand globally, though its user growth faced a setback in early 2023 when an Italian regulatory intervention forced the company to disable its romantic roleplay features. Character.AI operates on a different axis, positioning itself as a multi-persona creative platform rather than a singular companion product, which provides regulatory insulation and broader demographic reach.

Inflection AI's Pi built a loyal base around its low-pressure conversational style before the Microsoft talent acquisition in 2024. Baidu's ERNIE-powered companion integrations and ByteDance's experimental companion features within Douyin signal that the largest consumer technology firms view this category as an extension of their engagement and advertising ecosystems. The underlying LLM infrastructure is increasingly dominated by a small number of model providers, creating a dependency dynamic where differentiation must be achieved at the application, memory, and personalization layer rather than at the model layer itself.

Recent Developments

- 2024: Snap Inc. expanded My AI with persistent memory features, enabling contextual conversations across sessions for its 750 million user base, setting a new standard for embedded companion experiences within social platforms.

- 2024: Google entered a licensing arrangement with Character.AI, providing infrastructure support and signaling that hyperscalers view companion AI as a strategic consumer engagement layer worth investing in at the platform level.

- 2023: Microsoft acquired key Inflection AI talent, integrating Pi's conversational design philosophy into Microsoft Copilot's consumer-facing features and accelerating the enterprise companion roadmap.

- 2023: The Mozilla Foundation analysis rated the majority of tested AI companion apps poorly on privacy standards, triggering a wave of product updates from leading vendors to add data transparency dashboards and consent management tools.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | AI Companion App Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $37.20B |

| Market Size (2033) | $227.21B |

| CAGR | 29.500% |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East & Africa |

| Segments Covered | Product Type, Voltage Rating, Application, And Region |

| Companies Covered | Luka Inc. (Replika), Character.AI, Snap Inc. (My AI), Xiaoice (Microsoft spinoff), Wysa, Woebot Health, Inflection AI (Pi), Gatebox Inc., Baidu (ERNIE Companion), ByteDance (Companion AI) |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Frequently Asked Questions — AI Companion App Market

You May Also Like

Specialist in ICT & Electronics market intelligence.

Schedule Free Analyst Call