Port Equipment Market Overview & Analysis

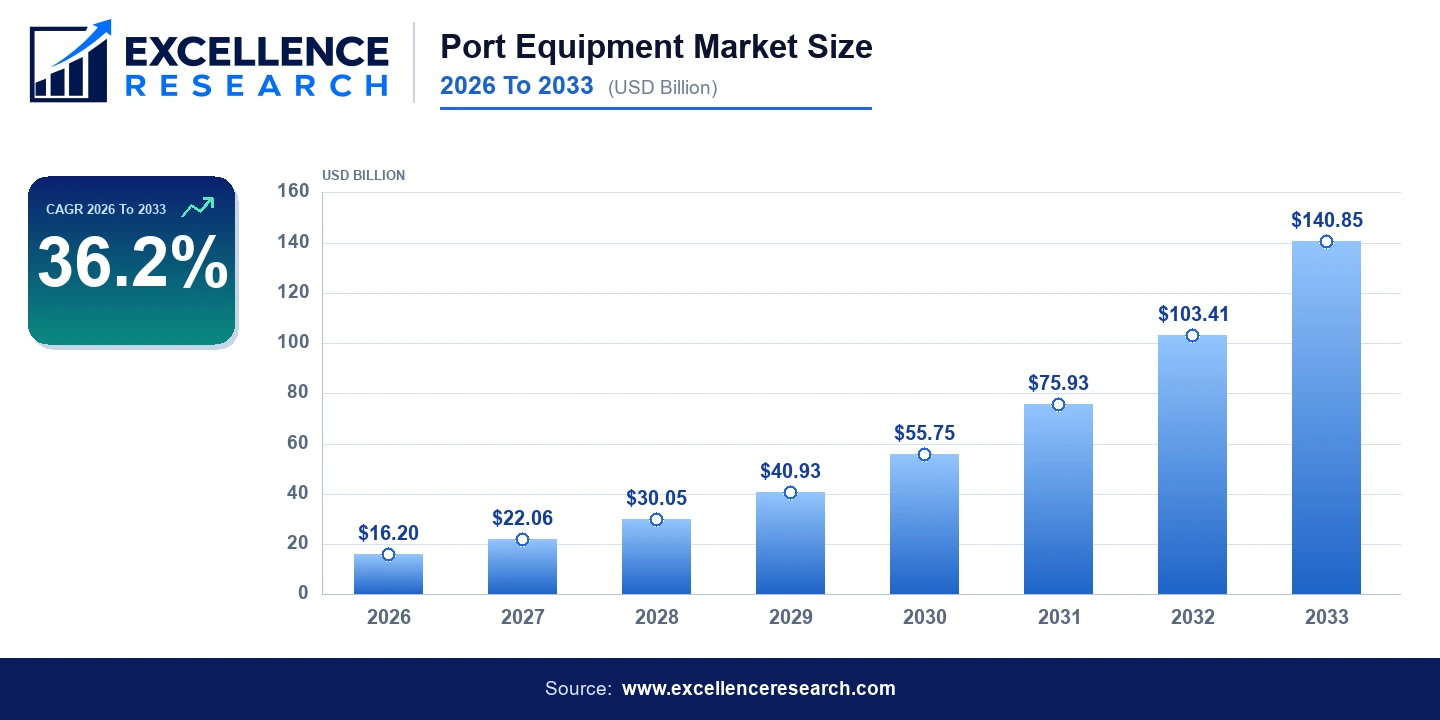

The Port Equipment Market size was valued at USD 16.2 billion in 2026 and is projected to reach USD 140.85 billion by 2033, expanding at a compound annual growth rate of 36.2% over the forecast period. This remarkable trajectory reflects accelerating global trade volumes, widespread terminal modernization programs, and the rapid adoption of autonomous and electrified handling solutions across more than 45 countries. The Port Equipment Market share is being actively contested by both established European manufacturers and fast-growing Asian conglomerates, as port operators prioritize throughput efficiency, decarbonization compliance, and reduced labor dependency. Rising container traffic through major transhipment hubs in Asia, Europe, and North America continues to underpin capital expenditure cycles that favor high-capacity, technology-integrated equipment platforms.

Key Report Takeaways

- By Operation: Conventional operation held the largest share in 2026 given the installed base at legacy terminals worldwide, while Autonomous operation is the fastest-growing segment as ports in Singapore, Rotterdam, and Qingdao expand automated terminal infrastructure.

- By Power Source: Diesel-powered equipment dominated revenue in 2026 due to its established refueling infrastructure, while Electric power is the fastest-growing category driven by decarbonization mandates in the European Union and China's green port initiatives.

- By Equipment Type: Container Handlers held the largest Port Equipment Market share in 2026, while Terminal Tractors are the fastest-growing equipment type owing to surging demand for automated guided vehicle deployments at greenfield container terminals.

Market Drivers

Global container throughput surpassed 900 million twenty-foot equivalent units in 2023 and continues to grow at approximately 3.5% annually, creating persistent demand for high-capacity equipment. Countries across Southeast Asia, the Middle East, and West Africa are investing heavily in new port infrastructure, with projects such as the USD 3.3 billion King Salman International Complex in Saudi Arabia and Vietnam's Lach Huyen deep-water port expansion directly generating procurement cycles for reach stackers, heavy forklifts, and container handlers. This infrastructure pipeline is a principal driver identified in every credible Port Equipment Market report published in recent years, reinforcing the bullish Port Equipment Market forecast through 2033.

Regulatory pressure is a second major driver. The International Maritime Organization's Carbon Intensity Indicator framework and the European Union's Fit for 55 package are compelling terminal operators to retire diesel-only fleets in favor of hybrid and fully electric alternatives. Konecranes Abp reported that orders for electric rubber-tyred gantry cranes constituted more than 60% of its RTG backlog in 2023, illustrating how policy alignment is reshaping procurement decisions. Additionally, port labor shortages in the United States, Germany, and South Korea are accelerating investments in autonomous terminal tractors and automated stacking cranes, broadening the addressable market for companies such as ABB, Siemens AG, and Gaussin Group that supply the control architecture underlying autonomous operations.

Segment Analysis

By Operation: Conventional equipment still represents the backbone of global port operations in 2026, accounting for the majority of installed fleets at the approximately 5,400 commercial ports worldwide. However, the Autonomous segment is expanding at a substantially higher rate as terminal operators quantify labor cost savings of 25 to 30% and throughput gains of up to 20% at fully automated facilities such as the COSCO-backed Yangshan Phase IV terminal in Shanghai. Emerson Electric Co. and ABB are supplying industrial automation platforms that integrate sensor fusion, machine vision, and predictive maintenance into autonomous equipment ecosystems, enabling operators to justify the higher upfront capital cost.

By Power Source: Diesel remains dominant in 2026, particularly across terminals in developing economies where grid reliability is insufficient to support large-scale electric fleets. Nevertheless, the Electric segment is forecast to record the highest Port Equipment Market growth rate through 2033 as battery energy density improvements and falling lithium-ion costs close the total cost of ownership gap. Hybrid solutions, offered by players such as Kalmar and Liebherr Group, are gaining traction as a bridging technology, delivering fuel savings of 30 to 40% without requiring comprehensive grid infrastructure upgrades. Toyota Material Handling is investing in hydrogen fuel cell terminal tractors as a premium zero-emission alternative in markets where extended duty cycles challenge battery endurance.

By Equipment Type: Container Handlers, including ship-to-shore cranes and rubber-tyred gantry cranes, generated the largest revenue contribution in 2026, reflecting the central role these machines play in loading and unloading ocean-going vessels. Shanghai Zhenhua Heavy Industries, commonly known as ZPMC, commands a globally dominant position in ship-to-shore cranes. Reach Stackers and Heavy Forklifts serve critical intermodal logistics functions and are supplied by Cargotec Corporation, CVS FERRARI, and Anhui Heli Co. Ltd. at highly competitive price points. Terminal Tractors are emerging as the fastest-growing equipment type, with Gaussin Group and LONKING HOLDINGS LIMITED advancing hydrogen and battery-electric variants that align with smart port automation mandates in Europe and China.

Regional Analysis

Asia-Pacific dominates the Port Equipment Market with approximately 42% revenue share in 2026, anchored by China, South Korea, Japan, and rapidly expanding Southeast Asian economies. China alone accounted for seven of the world's ten busiest container ports in 2023, sustaining continuous procurement by operators such as COSCO Shipping Ports and China Merchants Port Holdings. Sany Heavy Industry Co. Ltd. and LONKING HOLDINGS LIMITED benefit directly from domestic procurement preferences and government-backed port modernization subsidies. The Port Equipment Market analysis for this region consistently highlights state-directed capital allocation as a structural demand amplifier through 2033.

Europe represents the second-largest regional market, driven by the ambition of major port clusters in Rotterdam, Hamburg, Antwerp-Bruges, and Valencia to achieve carbon-neutral operations by 2030 to 2040. Konecranes Abp and Kalmar, both headquartered in Finland, hold strong regional market positions, while Siemens AG and ABB supply electrification and digitalization infrastructure. The European Commission's TEN-T corridor funding is directing billions of euros toward inland waterway and seaport upgrades, sustaining equipment demand even amid broader economic uncertainty across the Eurozone. Regulatory stringency in this region is also setting global product development benchmarks that other markets progressively adopt.

North America is the third-largest market and is experiencing renewed investment following the U.S. Infrastructure Investment and Jobs Act, which allocated USD 17 billion specifically to ports, waterways, and ferries. The Port of Los Angeles, Port of Long Beach, and Port of New York and New Jersey are implementing multi-year capacity enhancement and electrification programs. American Crane and Equipment serves specialized heavy-lift requirements across U.S. military and industrial port facilities, while Toyota Material Handling and Kalmar compete aggressively in the terminal tractor and reach stacker segments. The Port Equipment Market 2033 outlook for North America is further strengthened by near-shoring trends that are increasing Gulf Coast and East Coast container volumes.

Competitive Landscape

The Port Equipment Market competitive landscape is moderately consolidated at the premium end and highly fragmented among mid-tier and regional suppliers. Kalmar, a Cargotec Corporation brand, and Konecranes Abp collectively command substantial share in the crane and container handler categories through decades of installed-base relationships, global service networks, and continuous R&D investment in electric and autonomous platforms. Shanghai Zhenhua Heavy Industries maintains an unrivaled position in ship-to-shore cranes, having supplied equipment to ports across more than 100 countries. Liebherr Group competes across mobile harbor cranes and heavy forklifts with a reputation for engineering precision and durability in harsh operating environments. Sany Heavy Industry Co. Ltd. is aggressively expanding its international footprint, leveraging cost competitiveness and an improving technology profile to challenge European incumbents in Southeast Asia, Africa, and the Middle East. ABB and Siemens AG occupy a distinct competitive tier as electrification and automation technology providers whose solutions are increasingly embedded in equipment offered by the hardware manufacturers, creating layered partnership and integration dynamics. The overall Port Equipment Market trends point toward consolidation through strategic acquisitions and joint ventures as companies seek full-spectrum offerings spanning hardware, software, and lifecycle service contracts.

Recent Developments

- 2024: Kalmar secured a contract valued at approximately USD 120 million to supply 24 automated stacking cranes and associated terminal operating system integration to the Port of Gdansk in Poland, reinforcing its leadership in European terminal automation.

- 2024: Konecranes Abp announced the commercial delivery of its first fully electric ship-to-shore crane powered entirely by renewable shore power to the Port of Gothenburg, Sweden, marking a milestone referenced in multiple editions of the Port Equipment Market report for its demonstration effect on industry electrification timelines.

- 2023: Gaussin Group launched its hydrogen-powered automated terminal tractor at the TOC Europe conference in Rotterdam, entering commercial pilot agreements with three Mediterranean port operators and signaling intensified competition in the zero-emission autonomous tractor segment.

- 2023: Sany Heavy Industry Co. Ltd. completed a strategic partnership with a major Middle Eastern port developer to supply heavy forklifts, reach stackers, and container handlers for three greenfield terminals along the Red Sea, a deal reflecting the geographic expansion central to the Port Equipment Market growth narrative for the 2023 to 2033 period.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Port Equipment Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $16.20B |

| Market Size (2033) | $140.85B |

| CAGR | 36.200% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Operation, Power, And Equipment Type |

| Companies Covered | Kalmar, Liebherr Group, Konecranes Abp, Sany Heavy Industry Co. Ltd., Shanghai Zhenhua Heavy Industries, Emerson Electric Co., Toyota Material Handling, Cargotec Corporation, Anhui Heli Co. Ltd., Gaussin Group, CVS FERRARI, LONKING HOLDINGS LIMITED and others |

Segmentation Covered

Key Companies Profiled (15)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Port Equipment Market

You May Also Like

Specialist in Market Research market intelligence.

Schedule Free Analyst Call