Anti-wrinkle Products Market Overview & Analysis

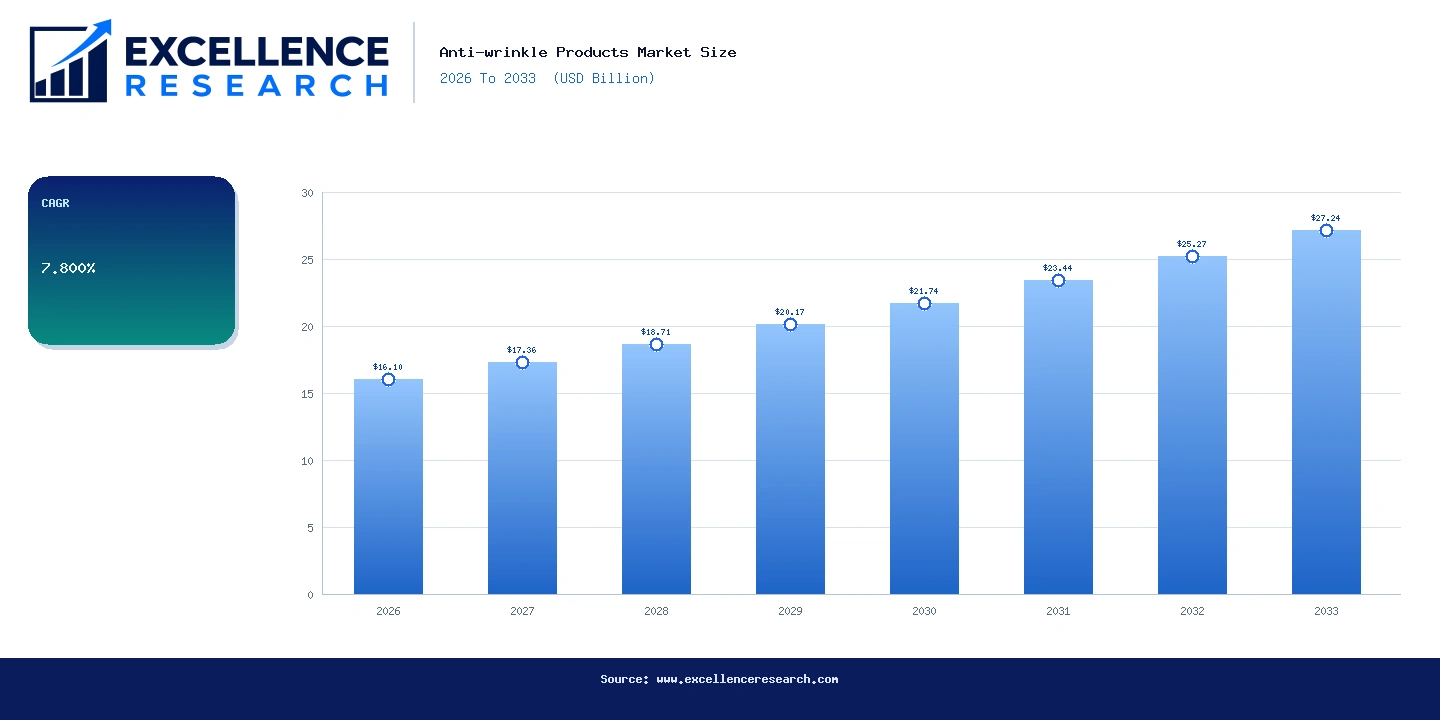

The global anti-wrinkle products market is valued at $16.1 billion in 2026 and is projected to reach $27.24 billion by 2033, advancing at a compound annual growth rate of 7.8% over the forecast period. This sustained expansion reflects intensifying consumer demand for clinically validated skincare formulations, a rapidly aging global population, and significant product innovation from leading dermocosmetic and pharmaceutical-grade brands operating across more than 45 countries. The market encompasses a broad spectrum of topical formulations, including creams and oils, distributed through specialty retail channels and pharmacy networks worldwide. Increasing consumer awareness of preventive skincare regimens among millennials and Gen Z demographics, combined with growing medical tourism and dermatologist-endorsed product usage, is reinforcing growth well beyond traditional mature-consumer segments.

Key Report Takeaways

- By Active Ingredient: Retinoids held the largest share of the active ingredient segment, accounting for approximately 38% of ingredient-driven revenue in 2025, owing to decades of clinical validation and strong endorsements from dermatologists globally; Glycolic Acid is the fastest-growing active ingredient sub-segment, driven by consumer adoption of chemical exfoliation routines and the proliferation of at-home peel products from brands such as RoC Skincare and Neutrogena.

- By Product Type: Creams dominated the product segment with over 71% revenue share in 2025, supported by widespread consumer familiarity and the format's compatibility with high-concentration active ingredient delivery; Oils are the fastest-growing product type, propelled by the clean beauty movement and formulations from REN Clean Skincare and Kiehl's Since 1851 that combine retinoid and botanical oil actives.

- By Distribution Channel: Pharmacies and Drugstores held the largest distribution channel share, representing roughly 44% of total market revenue in 2025, anchored by trust in pharmacy-adjacent dermocosmetic brands such as La Roche-Posay Laboratoire Dermatologique, CeraVe, and Vichy Laboratoires; Specialty Stores are the fastest-growing distribution channel, fueled by the expansion of Sephora and Ulta Beauty retail networks and their curated premium skincare assortments.

Market Drivers

The primary driver of anti-wrinkle product demand is the accelerating demographic shift toward older populations across North America, Europe, and Asia-Pacific. According to the United Nations, the global population aged 60 years and older is projected to exceed 1.4 billion by 2030, creating a structurally expanding consumer base with documented disposable income allocated toward personal care. This demographic increasingly seeks prescription-adjacent, over-the-counter formulations that deliver measurable skin renewal results, directly benefiting retinoid-based product lines from companies such as Galderma S.A., which markets Differin adapalene gel, and The Estée Lauder Companies Inc., whose Advanced Night Repair serum franchise generates over $1 billion in annual retail sales. The intersection of aging demographics and premiumization in skincare is translating into higher average selling prices per unit, with prestige anti-wrinkle products growing at a rate nearly 1.5 times that of mass-market equivalents.

A second critical driver is the surge in dermatologist-to-consumer digital communication through social media platforms, telehealth skincare consultations, and evidence-based content marketing. Brands such as CeraVe and La Roche-Posay Laboratoire Dermatologique have built substantial engagement by partnering directly with board-certified dermatologists who validate ingredient efficacy to audiences numbering in the tens of millions across YouTube and TikTok. This credibility-driven marketing model has elevated consumer understanding of ingredients such as Lactic Acid, Citric Acid, and peptide complexes, accelerating trial and repeat purchase cycles. Simultaneously, the growing global e-commerce infrastructure, with platforms like Amazon, Tmall, and brand-owned direct-to-consumer storefronts, is reducing geographic barriers and enabling brands such as Groupe Clarins and Shiseido Co., Ltd. to reach consumers in emerging markets across Southeast Asia, Latin America, and the Middle East with premium anti-aging propositions.

Segment Analysis

By Active Ingredients: Retinoids remain the gold-standard active ingredient category in anti-wrinkle formulations, supported by over 40 years of peer-reviewed clinical evidence demonstrating measurable reductions in fine lines, uneven pigmentation, and collagen degradation. Brands including RoC Skincare, Neutrogena, and La Roche-Posay Laboratoire Dermatologique have built flagship product lines around retinol and retinaldehyde concentrations ranging from 0.025% to 1.0%, catering to both entry-level and advanced users. Glycolic Acid, an alpha-hydroxy acid derived from sugarcane, is gaining rapid traction as a complementary or standalone anti-wrinkle active, particularly in serums and toning products marketed by Origins Natural Resources, Inc. and Clinique Laboratories. Lactic Acid is carving a niche among consumers with sensitive skin types, with formulations positioned as gentler alternatives to Glycolic Acid, while Citric Acid serves increasingly as a pH adjuster and antioxidant booster within multi-active complexes developed by Vichy Laboratoires and Life Extension.

By Product Type: Creams represent the foundational format of the anti-wrinkle category, with moisturizer-based delivery systems enabling high concentrations of actives to be applied with skin-barrier-reinforcing emollient bases. POND'S Age Miracle and OLAY Regenerist remain among the most recognizable cream franchises globally, with combined retail presence across more than 80 countries. The cream segment benefits from strong repeat-purchase behavior, as consumers typically integrate anti-wrinkle creams into twice-daily skincare routines, generating consistent revenue streams for manufacturers. The oil segment is emerging as a high-growth opportunity, with premium players such as Kiehl's Since 1851, which markets its Midnight Recovery Concentrate, and REN Clean Skincare leading the adoption of facial oils that blend retinoid actives with omega-rich botanical carriers including rosehip, squalane, and marula oil. The oil format commands an average retail price premium of approximately 25% to 40% over comparable cream formulations, improving gross margin profiles for brands operating in this sub-category.

By Distribution Channel: Pharmacies and Drugstores represent the most trusted point of purchase for anti-wrinkle products, benefiting from the perceived clinical credibility associated with pharmacy environments. The strategic positioning of dermocosmetic brands such as CeraVe, Vichy Laboratoires, and La Roche-Posay Laboratoire Dermatologique within pharmacy aisles, often adjacent to prescription skincare and supported by pharmacist recommendation programs, drives substantial conversion. Specialty Stores including Sephora, Space NK, and Ulta Beauty are rapidly expanding their anti-aging assortments, incorporating prestige and clinical brands such as No7 Beauty Company (Walgreens Boots), Groupe Clarins, and The Estée Lauder Companies Inc. These specialty retail environments emphasize personalized consultation, sampling, and loyalty programs that generate elevated customer lifetime value compared to mass retail channels. The ongoing shift toward omnichannel retail strategies, with brands simultaneously investing in in-store experiences and direct-to-consumer digital platforms, is reshaping distribution economics across the category.

Regional Analysis

North America is the largest regional market for anti-wrinkle products, accounting for approximately 34% of global revenue in 2025. The United States represents the dominant national market within the region, underpinned by high per-capita spending on personal care, a mature and sophisticated consumer base, and robust pharmacy retail infrastructure anchored by Walgreens, CVS, and Target. Key growth contributors include the market leadership of Neutrogena Rapid Wrinkle Repair, OLAY Regenerist Micro-Sculpting Cream, and CeraVe Skin Renewing Night Cream, all of which command significant shelf space and consumer mindshare. The region also benefits from strong telehealth and dermatologist-referral channels that direct consumers toward clinically validated retinoid formulations, and the presence of major research and development hubs for companies such as The Estée Lauder Companies Inc., headquartered in New York, and Clinique Laboratories, which conducts ongoing dermatological efficacy testing at dedicated research centers.

Europe is the second-largest regional market, representing approximately 28% of global market value in 2025. France serves as the intellectual and commercial epicenter of the European anti-wrinkle segment, home to L'ORÉAL GROUPE, Groupe Clarins, and Vichy Laboratoires, which collectively generate billions of euros in anti-aging product revenue annually. Germany, the United Kingdom, and Italy are significant national markets, with No7 Beauty Company (Walgreens Boots) maintaining particularly strong penetration in the UK through its clinical retinol serums. European regulatory frameworks under the EU Cosmetics Regulation 1223/2009 impose strict concentration limits on retinoids, capping retinol at 0.3% in face products as of 2024, which is prompting reformulation investment across the region and creating differentiation opportunities for brands capable of demonstrating efficacy within revised guidelines. The European market also demonstrates above-average adoption of clean and sustainable anti-wrinkle formulations, benefiting REN Clean Skincare and Origins Natural Resources, Inc.

Asia-Pacific is the fastest-growing regional market, projected to advance at a CAGR of approximately 9.2% between 2026 and 2033, driven by demographic aging in China and Japan, rising middle-class purchasing power across South Korea, India, and Southeast Asia, and deeply embedded cultural investment in skincare regimens. Japan and South Korea are technologically sophisticated markets where Shiseido Co., Ltd. maintains a leadership position through its Benefiance and Vital Perfection anti-aging lines, with domestic consumers demonstrating willingness to pay premium prices for proven efficacy. China represents the most significant growth opportunity in the region, with the anti-wrinkle segment benefiting from the explosion of e-commerce on platforms such as Tmall and JD.com and the

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Anti-wrinkle Products Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $16.10B |

| Market Size (2033) | $27.24B |

| CAGR | 7.800% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Active Ingredients, Product, And Distribution Channel |

| Companies Covered | L’ORÉAL GROUPE, OLAY, CeraVe, Neutrogena, RoC Skincare, POND'S, No7 Beauty Company (Walgreens Boots), La Roche-Posay Laboratoire Dermatologique, REN Clean Skincare, Galderma S.A., Clinique Laboratories, Shiseido Co., Ltd and others |

Segmentation Covered

Key Companies Profiled (18)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Anti-wrinkle Products Market

You May Also Like

Specialist in Beauty and Personal Care market intelligence.

Schedule Free Analyst Call