Skin Care Products Market Overview & Analysis

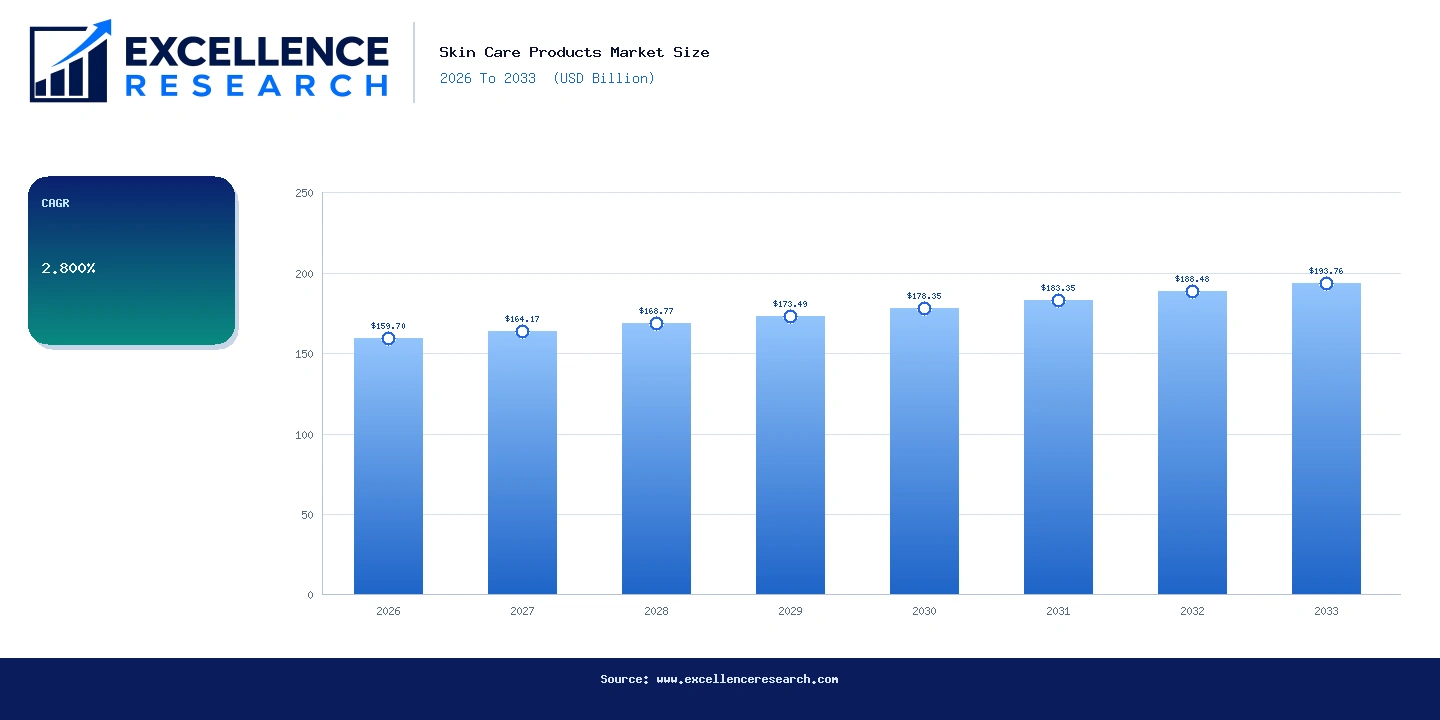

The global skin care products market is valued at USD 159.7 billion in 2026 and is projected to reach USD 193.76 billion by 2033, expanding at a compound annual growth rate of 2.8% over the forecast period. This steady growth trajectory reflects sustained consumer investment in personal care routines, rising dermatological awareness, and accelerating product innovation across both mass-market and prestige tiers. The market spans over 45 countries, with meaningful demand originating from mature markets in North America and Western Europe as well as high-growth corridors across Asia Pacific, Latin America, and the Middle East. Structural tailwinds including aging demographics, greater male grooming adoption, and the proliferation of e-commerce channels continue to expand the addressable consumer base for leading manufacturers such as L'Oréal S.A., Unilever, and Beiersdorf AG.

Key Report Takeaways

- By Gender: Female consumers held the largest revenue share at approximately 68% in 2026, while the male segment is the fastest-growing category, driven by expanding men's grooming portfolios from brands including Beiersdorf AG's NIVEA Men and Procter and Gamble's Gillette skincare line.

- By Product: Face Creams and Moisturizers dominated product revenue, accounting for roughly 28% of total market value in 2026, while Sunscreen is the fastest-growing product segment, propelled by rising UV awareness and regulatory mandates in markets including Australia, South Korea, and Brazil.

- By Distribution Channel: Supermarkets and Hypermarkets retained the leading distribution share globally, while the Online channel is the fastest-growing, with platforms such as Amazon, Tmall, and brand direct-to-consumer websites collectively capturing an increasing proportion of annual skin care purchases.

- By Price Range: Mid-Range products commanded the largest share of consumer spending in 2026, while the Premium segment is the fastest-growing price tier, supported by rising disposable incomes in Asia Pacific and a demonstrated consumer willingness to invest in clinically positioned formulations.

Market Drivers

Rising consumer awareness of skin health and preventive dermatology is one of the most consequential demand drivers in the global skin care market. Dermatologist-endorsed content on platforms including TikTok, YouTube, and Instagram has democratized access to ingredient-level education, prompting consumers across age groups to adopt multi-step routines featuring serums, SPF moisturizers, and targeted treatments. A 2024 consumer survey conducted across the United States, United Kingdom, and China found that 61% of respondents increased their average monthly skin care spending compared to three years prior, with active ingredients such as retinol, niacinamide, and hyaluronic acid cited as primary purchase motivators. This informed consumer base creates favorable conditions for premium pricing and repeat purchase cycles, benefiting companies including Shiseido Co., Ltd. and Johnson and Johnson, Inc.

Urbanization and demographic shifts are reinforcing long-term volume growth. The global population aged 50 and above is projected to reach 2.1 billion by 2030, according to United Nations data, and this cohort demonstrates above-average spending on anti-aging formulations including eye creams, firming serums, and broad-spectrum sunscreens. Simultaneously, rapidly expanding urban middle-class populations in India, Indonesia, Vietnam, and Nigeria are entering the formal skin care market for the first time, prioritizing cleansers, moisturizers, and sun protection products at economy and mid-range price points. Manufacturers are responding with localized product development, including Unilever's region-specific SKUs under the Pond's and Vaseline brands and L'Oréal's dedicated research center in Mumbai focused on South Asian skin tones and humidity-related concerns.

Segment Analysis

By Gender: The female segment generated approximately USD 108.6 billion in market value in 2026, underpinned by broad category engagement spanning facial moisturizers, eye creams, toners, and body lotions. The male segment, while currently smaller in absolute terms, is expanding at a meaningfully faster rate as cultural norms around male grooming evolve across North America, Europe, and East Asia. Procter and Gamble reported double-digit growth in its men's skin care subcategory in fiscal 2023, and Beiersdorf AG's NIVEA Men franchise reached annual net sales exceeding EUR 700 million globally. Dedicated men's skin care lines from prestige labels including Clinique, Lab Series, and Kiehl's are further legitimizing daily facial care regimens among male consumers aged 25 to 45.

By Product: Face Creams and Moisturizers represent the single largest product category, reflecting universal consumer demand for hydration and barrier protection across all geographies and demographics. Cleansers and Face Wash rank as the second largest category by volume, with waterless and micellar formats gaining significant traction in water-scarce markets and among environmentally conscious consumers. Sunscreen is attracting disproportionate investment from both established players and independent brands, with the global SPF segment projected to grow at a rate exceeding 4.5% annually through 2033. Body Creams and Moisturizers generate substantial revenue in tropical climates and colder markets alike, while Shaving Lotions and Creams remain an important subcategory driven by male grooming penetration in emerging economies including Brazil, Mexico, and Nigeria.

By Distribution Channel: Supermarkets and Hypermarkets including Walmart, Carrefour, and Tesco collectively serve as the primary point of purchase for mass-market skin care globally, offering consumers the ability to trial products and access promotional pricing. Pharmacy and Drugstore channels, including CVS, Walgreens, Boots, and DM Drogerie Markt, have grown in strategic importance as consumers increasingly seek dermatologist-recommended brands such as CeraVe, owned by L'Oréal, and Eucerin, owned by Beiersdorf AG. The Online distribution channel is exhibiting the strongest structural growth, with skin care representing one of the top three personal care categories by e-commerce penetration. Convenience Stores serve a differentiated role in high-density Asian urban markets, particularly in Japan and South Korea, where premium single-serve formats and travel-sized SKUs drive impulse purchases.

By Price Range: Economy-priced products maintain broad relevance in price-sensitive markets across South and Southeast Asia, sub-Saharan Africa, and parts of Latin America, where brands including Unilever's Pond's, Avon Products, and Colgate-Palmolive's Palmolive compete on accessibility and value. Mid-Range products represent the largest revenue segment by price tier, with brands including Neutrogena, Olay, and NIVEA occupying the central positioning in most retail environments globally. The Premium segment, encompassing brands such as Shiseido's CLÉ DE PEAU BEAUTÉ, L'Oréal's Lancôme, and Estée Lauder's La Mer, is capturing a growing share of consumer wallet in China, South Korea, Japan, and Gulf Cooperation Council markets, where gifting culture and prestige brand affiliation drive outsized average transaction values.

Regional Analysis

Asia Pacific is the single largest regional market for skin care products, accounting for an estimated 38% of global market value in 2026. China, Japan, South Korea, and India are the four leading national markets in the region. South Korea's influence extends far beyond its domestic market, as K-beauty innovation in sheet masks, essences, and sunscreen formats has shaped product development priorities for multinational corporations worldwide. China represents the most significant near-term growth opportunity, with the country's skin care market valued at approximately USD 30 billion in 2026 and expanding at above-market rates fueled by domestic consumption upgrades and the popularity of domestic brands including Proya and Winona alongside global players including L'Oréal, Shiseido, and Estée Lauder.

North America is the second largest regional market, with the United States accounting for the majority of regional revenue at an estimated USD 24.5 billion in 2026. The United States skin care market is characterized by high per-capita spending, a mature retail infrastructure, and a rapidly evolving clean beauty and dermocosmetics segment. The direct-to-consumer channel has gained significant traction in North America, with brands including Curology, Paula's Choice, and Tatcha building substantial revenue bases without reliance on traditional retail. Canadian and Mexican markets are growing steadily, supported by demographic expansion and increasing alignment with United States consumption trends.

Europe represents the third largest regional market, with Germany, France, the United Kingdom, and Italy accounting for the majority of European skin care revenue. Germany is the leading European national market, supported by a deeply embedded drugstore retail culture anchored by chains including DM and Rossmann, which provide distribution infrastructure for brands owned by Beiersdorf AG and other regional champions. France benefits from the global authority of its luxury and prestige beauty sector, with L'Oréal headquartered in Clichy and operating brands across every price tier. Regulatory developments within the European Union, including restrictions on certain synthetic ingredients and mandatory sustainability reporting requirements under the European Green Deal, are accelerating reformulation activity across the region's supply chain.

Competitive Landscape

The global skin care products market is moderately consolidated at the top tier, with the five largest companies including L'Oréal S.A., Unilever, Procter and Gamble, Beiersdorf AG, and Shiseido Co., Ltd. collectively accounting for an estimated 42% of global market revenue in 2026. L'Oréal S.A. maintains the leading competitive position globally, supported by a portfolio spanning 36 international brands across the Consumer Products, L'Oréal Luxe, Professional Products, and Active Cosmetics divisions. The company reported consolidated net sales of EUR 41.18 billion in fiscal 2023, with skin care representing its largest product category. Beiersdorf AG leverages the NIVEA masterbrand, the world's best-selling skin care brand by retail value, alongside the Eucerin and La Prairie brands to address mass, pharmacy, and ultra-premium consumer segments simultaneously. Johnson and Johnson, Inc. continues to invest in its dermatology-adjacent skin care portfolio following the separation of its consumer health division into Kenvue Inc. in

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Skin Care Products Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $159.70B |

| Market Size (2033) | $193.76B |

| CAGR | 2.800% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Gender, Product, Distribution Channel, And Price Range |

| Companies Covered | L’Oréal S.A., Beiersdorf AG, Shiseido Co., Ltd., Procter & Gamble (P&G), Unilever, Johnson & Johnson, Inc., Avon Products, Inc., Coty Inc., Colgate-Palmolive Company, Revlon |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Skin Care Products Market

You May Also Like

Specialist in Beauty and Personal Care market intelligence.

Schedule Free Analyst Call