Consumer Electronics Market Overview & Analysis

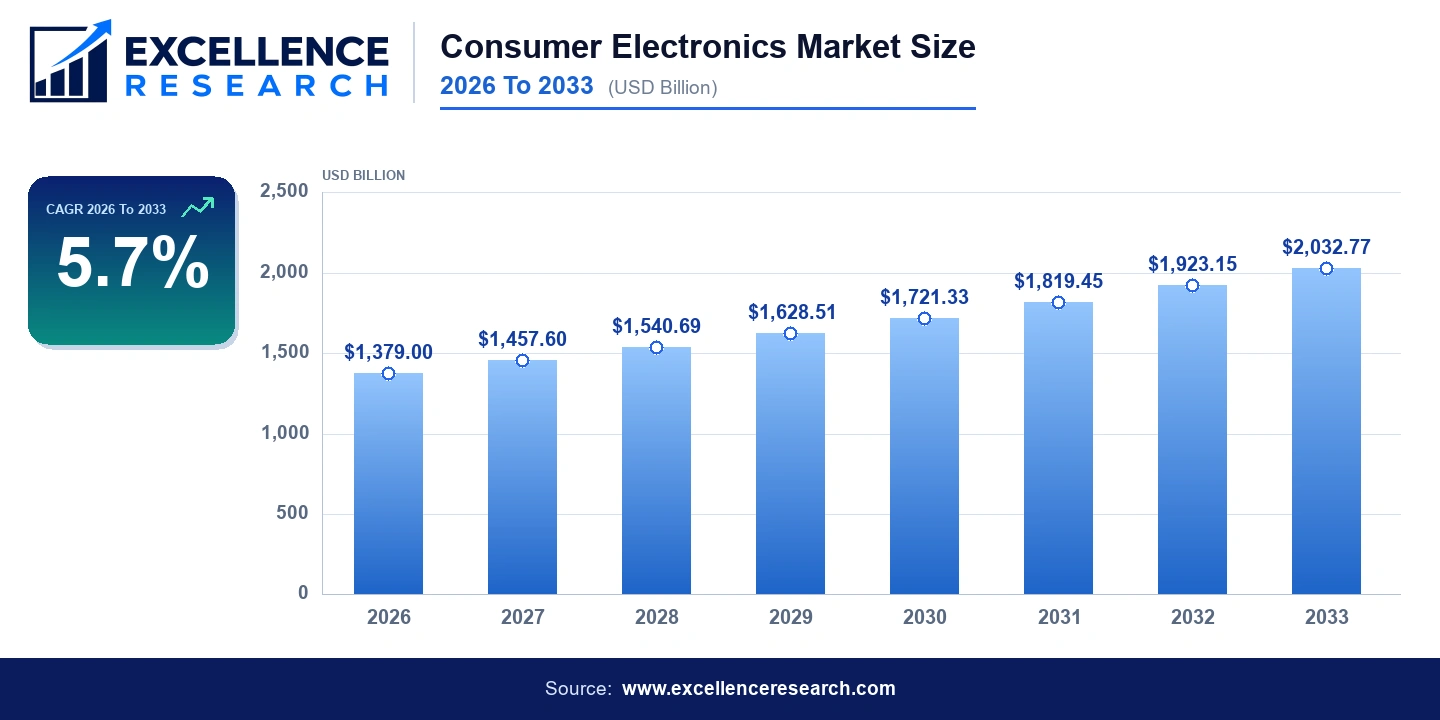

The Consumer Electronics Market size was valued at USD 1,379 billion in 2026 and is projected to reach USD 2,032.77 billion by 2033, expanding at a compound annual growth rate of 5.7% over the forecast period. This Consumer Electronics Market share is distributed across a highly fragmented competitive base spanning more than 45 countries, with dominant positions held by established technology giants including Samsung Electronics Co., Ltd., Apple Inc., and Sony Corporation. Rising disposable incomes across emerging economies, accelerating 5G network deployment, and deepening consumer demand for connected home ecosystems are the foundational forces sustaining this trajectory.

According to the latest Consumer Electronics Market report compiled by Excellence Research, the market continues to demonstrate resilience despite macroeconomic headwinds, supply chain normalization post-2022, and shifting consumer preferences toward premium, energy-efficient devices. The integration of artificial intelligence into personal computing, imaging, and mobile platforms is redefining product value propositions and driving replacement cycles at a pace not seen since the smartphone revolution of the early 2010s.

Key Report Takeaways

- By Product, Smartphones: Smartphones held the largest revenue share at approximately 38% in 2026, driven by continuous hardware upgrades and 5G adoption; Tablets represent the fastest-growing product segment with an estimated CAGR of 7.2% through 2033, fueled by hybrid work and education demand.

- By Sales Channel, Offline: Offline retail channels retained the largest share at roughly 54% of total Consumer Electronics Market revenue in 2026; Online channels are the fastest-growing distribution route, recording a CAGR exceeding 8.1% as e-commerce penetration deepens across Asia-Pacific, Latin America, and Eastern Europe.

Market Drivers

Global 5G subscriber counts surpassed 1.4 billion in 2023 according to GSMA Intelligence data, and are projected to exceed 5 billion by 2030. This infrastructure expansion is the single most powerful demand catalyst in the Consumer Electronics Market growth narrative. Handset replacement cycles are compressing in markets such as South Korea, Japan, and urban China as consumers upgrade to 5G-capable devices from Huawei Technologies Co., Ltd., Samsung Electronics, Apple Inc., and ZTE Corporation. Simultaneously, network slicing and ultra-low latency capabilities are enabling new categories of edge-computing devices, including augmented reality headsets and standalone industrial tablets, to enter the consumer mainstream.

The proliferation of remote and hybrid work arrangements has structurally elevated demand for laptops, external monitors, and webcam-equipped desktop systems. Dell Technologies reported a 14% year-over-year increase in commercial PC unit shipments in fiscal 2023, and Lenovo maintained its position as the world's largest PC vendor with a 24.1% global unit market share. E-reader adoption, while modest in absolute unit terms, has experienced renewed interest as literacy programs in India, Brazil, and sub-Saharan Africa integrate low-cost Micromax and local-brand devices into educational curricula. The Consumer Electronics Market analysis consistently highlights that rising middle-class populations in Asia-Pacific and Africa represent an underserved demand pool that will drive disproportionate volume growth through 2033.

Segment Analysis

By Product, Smartphones: Smartphones remain the anchor product category, accounting for an estimated USD 524 billion in revenue in 2026. Apple Inc. commanded a premium segment share of approximately 18% of global smartphone revenue, supported by the iPhone 15 series and the introduction of the A17 Pro chip. Samsung Electronics held a unit volume lead with approximately 22% global shipment share. Huawei Technologies Co., Ltd. demonstrated a remarkable recovery in China following the launch of its Mate 60 Pro series powered by a domestically fabricated 7-nanometer Kirin 9000S processor. HTC Corporation and Motorola Mobility LLC continue to serve mid-tier price segments across Latin America and Southeast Asia.

By Product, Tablets: Tablets generated approximately USD 78 billion in global revenue in 2026. Apple Inc. retained the leading position through its iPad Pro line, while Samsung Electronics offered the Galaxy Tab S9 series as a direct competitor in the premium Android segment. ASUSTeK Computer Inc. captured growing share in the budget and mid-range bracket, particularly in emerging markets where consumers seek affordable alternatives to laptops for educational and content-consumption use cases.

By Product, Television: The global Television segment approached USD 210 billion in 2026. LG Electronics and Samsung Electronics collectively accounted for over 40% of premium OLED and QLED television revenues. Sony Corporation's Bravia XR series maintained strong positioning in North America and Europe, leveraging its Cognitive Processor XR for picture quality differentiation. Panasonic Holdings Corporation continued to serve professional and high-end residential display markets in Japan and Western Europe.

By Product, Laptops and Notebooks: Laptops and notebooks represented approximately USD 195 billion of Consumer Electronics Market revenue in 2026. Lenovo led global shipments, followed by Dell Technologies, HP (Hewlett Packard Enterprise Development LP), Apple Inc., ASUSTeK Computer Inc., and Acer Inc. The segment is increasingly bifurcated between Arm-based processors, exemplified by Apple's M3 chip series, and Intel and AMD x86 architecture systems favored by enterprise procurement teams. Toshiba Corporation, operating through its Dynabook brand post-divestiture, maintained niche commercial laptop presence primarily in Japan.

By Product, Desktops: Desktops accounted for roughly USD 98 billion globally in 2026. While consumer desktop unit volumes have contracted steadily since 2018, gaming desktops and workstation-class systems produced by Dell Technologies, Lenovo, and ASUSTeK Computer Inc. have maintained value growth. The segment benefits from gaming market expansion, with global PC gaming revenues surpassing USD 38 billion annually.

By Product, E-readers: E-readers generated an estimated USD 14 billion in 2026. Amazon's Kindle platform dominates this segment globally, though the Consumer Electronics Market forecast for this category remains modest at a CAGR of approximately 3.1% through 2033. Micromax and regional players continue to compete in price-sensitive emerging markets.

By Product, Digital Cameras: Digital cameras produced revenues of approximately USD 32 billion in 2026. Canon Inc. and Nikon held the leading positions in the interchangeable-lens camera segment, with Canon's EOS R system and Nikon's Z-series mirrorless platforms driving unit and average selling price growth. Sony Corporation's Alpha series continued to gain professional market share. The broader point-and-shoot segment has essentially been cannibalized by smartphone camera advances, concentrating remaining volume in premium mirrorless and DSLR categories.

By Product, Hard Disk Drives: The Hard Disk Drive segment reached approximately USD 28 billion in 2026. Seagate Technology LLC and Toshiba Corporation are the two primary volume HDD suppliers following Western Digital's separation from its flash memory unit. Seagate's Mozaic 3 Plus platform, which utilizes heat-assisted magnetic recording to deliver 30-terabyte drives, underscores the segment's ongoing capacity growth even as solid-state drives capture share in consumer notebooks. Data center hyperscalers including Google LLC remain high-volume HDD customers for cold storage applications.

By Sales Channel, Offline: Physical retail, including carrier stores, consumer electronics chains, and big-box retailers, accounted for approximately 54% of Consumer Electronics Market revenue in 2026. Brand-controlled retail environments, such as Apple Stores and Samsung Experience Stores, generate above-average transaction values through accessory attachment and trade-in programs. In markets such as India and Southeast Asia, offline channels retain structural importance due to cash transaction prevalence and consumer preference for product demonstration before purchase.

By Sales Channel, Online: Online channels represented approximately 46% of 2026 revenue and are advancing at a CAGR of 8.1%, making this the fastest-growing distribution segment. Marketplace platforms operated by Amazon, JD.com, Flipkart, and Lazada collectively account for the majority of online consumer electronics transactions globally. Direct-to-consumer digital storefronts operated by Apple Inc., Dell Technologies, and Lenovo enable margin capture and richer customer data collection that competitors reliant on third-party retail cannot replicate.

Regional Analysis

Asia-Pacific dominates the Consumer Electronics Market with approximately 44% revenue share in 2026, generating an estimated USD 607 billion. China, Japan, South Korea, and India are the four largest national markets within this region. China alone accounts for roughly 21% of global consumer electronics expenditure, supported by a manufacturing base that hosts facilities for Samsung Electronics, Apple's Foxconn-managed supply chain, Huawei Technologies, Lenovo, and ZTE Corporation. India's Consumer Electronics Market growth rate is among the highest globally, driven by a smartphone user base that exceeded 750 million in 2023 and government production-linked incentive schemes attracting investment from Apple's contract manufacturers and Samsung Electronics.

North America held the second largest regional share at approximately 26% of global revenue in 2026, equivalent to roughly USD 358 billion. The United States is the dominant national market, characterized by high average selling prices, deep 5G penetration, and consumer openness to premium product tiers. Apple Inc. generates approximately 45% of its total hardware revenue from the United States. Dell Technologies, Google LLC, and Motorola Mobility LLC also anchor their primary commercial operations in North America. The Consumer Electronics Market forecast for North America projects a CAGR of approximately 4.8% through 2033, below the global average, reflecting market maturity and longer replacement cycles in mature product categories.

Europe represented approximately 18% of global Consumer Electronics Market revenue in 2026, or roughly USD 248 billion. Germany, the United Kingdom, and France are the three largest national markets. European demand is characterized by strong regulatory influence, including the European Union's mandate for universal USB-C charging compliance by 2024, which required product redesigns from Apple Inc. and other vendors. LG Electronics, Sony Corporation, and Panasonic Holdings Corporation maintain strong brand equity in European television and home appliance categories. The

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Consumer Electronics Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $1.38B |

| Market Size (2033) | $2.03B |

| CAGR | 5.700% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Product, And Sales Channel |

| Companies Covered | Apple Inc., Google LLC, Dell Technologies, Canon Inc., ACER INC., Panasonic Holdings Corporation, HEWLETT PACKARD ENTERPRISE DEVELOPMENT LP, HTC Corporation, Huawei Technologies Co., Ltd., LENOVO, LG ELECTRONICS, Micromax and others |

Segmentation Covered

Key Companies Profiled (20)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Consumer Electronics Market

You May Also Like

Specialist in Semiconductors and Electronics market intelligence.

Schedule Free Analyst Call