Solar-powered Security Camera Market Overview & Analysis

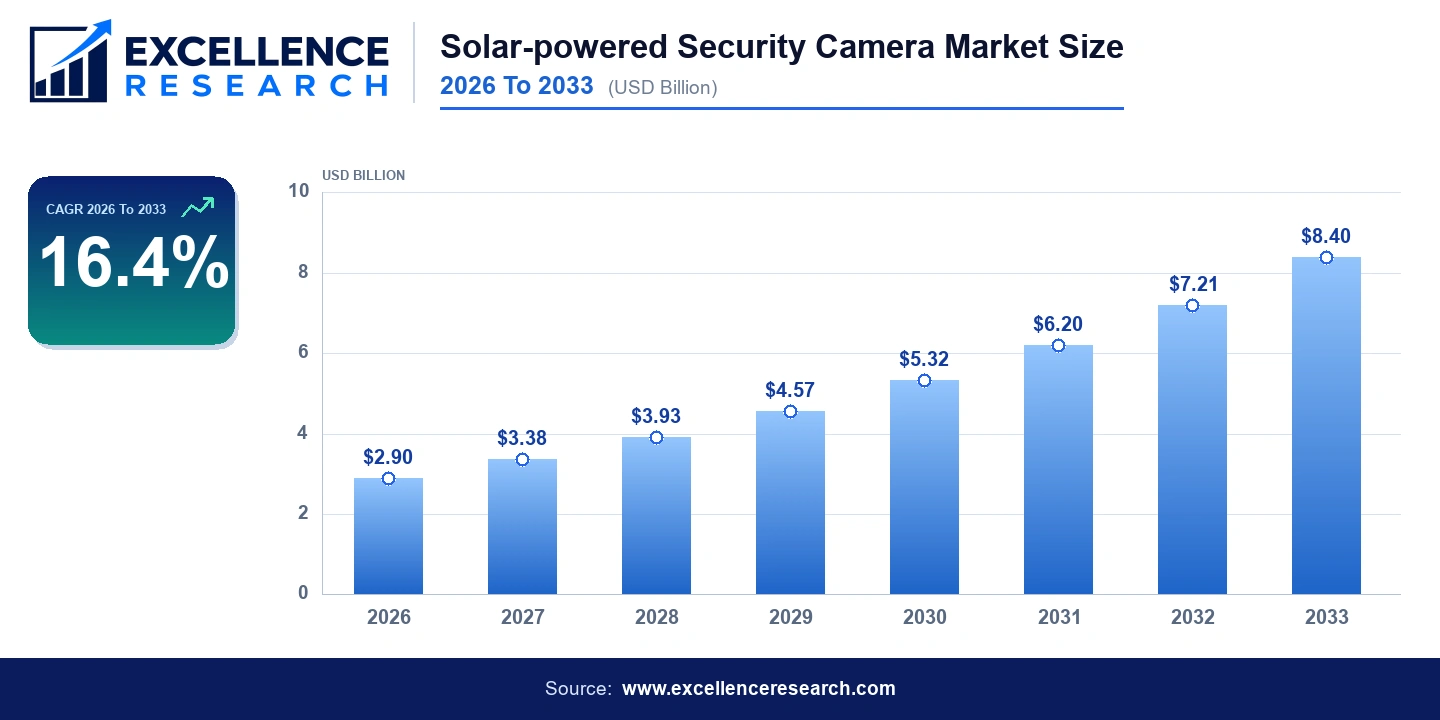

The Solar-powered Security Camera Market size was valued at approximately USD 2.9 billion in 2026 and is projected to reach USD 8.4 billion by 2033, expanding at a compound annual growth rate of 16.4% over the forecast period. This robust trajectory reflects accelerating adoption across residential neighborhoods, commercial facilities, and government-managed public infrastructure in more than 45 countries worldwide. The Solar-powered Security Camera Market share is being redistributed at a rapid pace as buyers shift from conventional wired systems toward wire-free, solar-integrated platforms that eliminate ongoing electricity costs and reduce installation complexity. Increasing grid unreliability in emerging economies, combined with tightening carbon-reduction mandates in developed markets, is making solar-powered surveillance a first-choice rather than a niche alternative. This Solar-powered Security Camera Market report captures that transition comprehensively, providing stakeholders with a granular understanding of product performance, connectivity preferences, distribution dynamics, and regional demand patterns through 2033.

Key Report Takeaways

- By Product: Bullet cameras held the largest share of the Solar-powered Security Camera Market in 2026 due to their cost efficiency and ease of outdoor deployment, while PTZ cameras are the fastest-growing product segment driven by demand for wide-area surveillance in critical infrastructure sites.

- By Connectivity: Wi-Fi-connected cameras dominated overall unit shipments in 2026 owing to broad router availability in urban and suburban residential settings, while cellular-connected cameras are the fastest-growing connectivity segment as remote and rural deployments multiply across agriculture, mining, and border security applications.

- By Distribution Channel: Offline channels, including specialty security dealers and big-box electronics retailers, held the largest revenue share in 2026, while online channels are the fastest-growing distribution route, supported by platform expansions on Amazon, Alibaba, and direct-to-consumer brand storefronts.

- By Application: Residential applications accounted for the leading share of the Solar-powered Security Camera Market in 2026, reflecting high consumer awareness and falling hardware prices, while critical infrastructure is the fastest-growing application segment as governments mandate camera coverage for energy grids, water treatment facilities, and transportation hubs.

Market Drivers

The primary engine behind Solar-powered Security Camera Market growth is the dramatic reduction in photovoltaic panel costs. Average solar module prices fell below USD 0.20 per watt in 2023 according to the International Renewable Energy Agency, making integrated solar panels a financially viable component rather than a premium add-on. Manufacturers including Hangzhou Hikvision Digital Technology Co., Ltd. and Shenzhen LS VISION Technology Co., Ltd. have responded by embedding higher-capacity lithium iron phosphate batteries alongside more efficient solar cells, extending continuous operation to 10 or more days without direct sunlight. This hardware improvement directly addresses the foremost objection historically raised by commercial buyers evaluating solar-powered surveillance alternatives.

Rising crime rates in urban centers across Latin America, Sub-Saharan Africa, and South and Southeast Asia are compelling municipal governments and private property owners to accelerate camera deployments in areas where running electrical conduit is prohibitively expensive or physically impractical. Simultaneously, smart city initiatives in South Korea, the United Arab Emirates, India, and the United Kingdom are channeling public spending into integrated surveillance networks, a policy shift that consistently favors solar-powered endpoints for their lower total cost of ownership. Advanced image processing capabilities, including 4K resolution, AI-driven motion classification, and license plate recognition now embedded in cameras from companies such as Milesight and Shenzhen LOYALTY-SECU Technology Co., LTD, further strengthen the value proposition and widen the addressable market for this technology category. The Solar-powered Security Camera Market analysis conducted for this report identifies these converging hardware, policy, and safety trends as mutually reinforcing growth catalysts through the forecast horizon.

Segment Analysis

By Product: Fixed cameras represent the entry-level tier of the market and command substantial unit volume, particularly among cost-sensitive residential buyers in North America and Europe who are installing their first outdoor cameras. Bullet cameras lead in revenue share because they balance affordability with weather resistance ratings of IP66 or IP67, making them suitable for a wide range of exterior mounting positions. Vendors such as Swann and Fantasia Trading LLC, operating its eufy brand, have standardized bullet-form solar cameras as their flagship consumer offerings. PTZ cameras, while carrying a higher average selling price of between USD 150 and USD 600 at retail, are gaining traction in commercial and public safety applications because a single unit can replace three to five fixed cameras through programmable patrol routes and remote operator control, delivering a compelling return on investment for security directors managing large perimeters.

By Connectivity: Wi-Fi cameras currently account for the majority of global shipments because residential and light-commercial buyers already possess broadband infrastructure and routers that support standard 2.4 GHz and 5 GHz protocols. However, the cellular segment is expanding at a notably faster rate because 4G LTE and 5G coverage now reaches previously inaccessible locations including agricultural fields, remote construction sites, and national park boundaries. Companies including Innotronik and Milesight have developed dedicated cellular solar camera product lines that use low-power LTE-M or NB-IoT modems to transmit video and alert data at substantially reduced power consumption compared to full-bandwidth cellular transmission, enabling smaller solar panels and battery packs while maintaining reliable connectivity.

By Distribution Channel: Offline retailers such as Home Depot in North America and Bunnings Warehouse in Australia remain influential because buyers purchasing cameras for residential installation frequently prefer to examine physical product packaging, assess build quality firsthand, and consult in-store staff before committing to a purchase. However, online platforms are growing faster because they facilitate direct price comparison, enable customer review verification, and allow smaller brands like Toucan Solution and Maizic to compete for national audiences without incurring retail shelf listing fees. Amazon alone listed more than 4,000 SKUs categorized under solar security cameras as of mid-2024, confirming that digital distribution has become a critical commercial battleground for brands of all sizes in this market.

By Application: Residential buyers purchase solar cameras primarily to monitor driveways, rear yards, and entry points, and this segment benefits from a large installed base of homeowners and renters who have already been introduced to smart home ecosystems through video doorbells and indoor cameras. Commercial applications including retail stores, warehouses, and construction sites are the second-largest application segment and typically involve multi-camera deployments that yield higher per-project revenue. Public safety applications, covering parks, transit stations, and street lighting integration, depend on government procurement cycles but are supported by multi-year funding frameworks in markets including the European Union and India. Critical infrastructure, encompassing substations, pipeline corridors, and water treatment plants, is registering the fastest application-level growth rate as regulatory bodies in the United States under FERC guidelines and in Europe under the EU Network and Information Security Directive mandate expanded perimeter monitoring that solar-powered systems can provide without requiring trenched electrical installations.

Regional Analysis

North America dominates the Solar-powered Security Camera Market with approximately 34% share in 2026, driven by high consumer spending on home security, a mature e-commerce infrastructure, and strong adoption of smart home platforms such as Amazon Alexa and Google Home that integrate with solar camera ecosystems. The United States accounts for the largest portion of regional revenue, with companies including TP-Link Systems Inc. and Fantasia Trading LLC actively marketing solar camera products through Amazon, Best Buy, and Costco. Federal investments under the Infrastructure Investment and Jobs Act have also directed funding toward surveillance upgrades at ports, border crossings, and transportation nodes, adding institutional demand on top of the substantial residential base.

Asia-Pacific represents the fastest-growing region in the Solar-powered Security Camera Market forecast period and held approximately 29% of global revenue in 2026. China is simultaneously the world's largest manufacturer and one of its fastest-growing domestic consumers of solar security cameras, with Hangzhou Hikvision Digital Technology Co., Ltd. and Shenzhen LS VISION Technology Co., Ltd. leveraging vertically integrated supply chains to price competitively in both home and export markets. India is projected to record a regional CAGR exceeding 19% through 2033, supported by the government's Safe City mission, Smart Villages program, and the rapid expansion of mobile broadband networks that make cellular-connected solar cameras viable in rural districts. Southeast Asian nations including Indonesia, Vietnam, and the Philippines are additional high-growth markets as urbanization and rising disposable incomes increase demand for residential security products.

Europe accounted for approximately 23% of the Solar-powered Security Camera Market in 2026 and is characterized by strict data privacy regulations under the General Data Protection Regulation that have shaped product feature sets, particularly around on-device video processing and local storage options rather than cloud-dependent architectures. Germany, the United Kingdom, and France are the three largest national markets within the region. European buyers show a pronounced preference for brands that can demonstrate GDPR-compliant data handling, creating a product differentiation opportunity for vendors willing to pursue regional certification. The region's ambitious renewable energy targets also create favorable policy environments for solar-powered devices across both residential and commercial segments, reinforcing demand growth at a projected regional CAGR of approximately 14% through 2033.

Competitive Landscape

The Solar-powered Security Camera Market is moderately fragmented, with a mix of large-scale surveillance technology conglomerates, mid-tier specialty manufacturers, and emerging consumer electronics brands competing across overlapping product tiers and distribution channels. Hangzhou Hikvision Digital Technology Co., Ltd. maintains a leading position in commercial and public safety segments through its extensive dealer network, broad product portfolio spanning entry-level to enterprise-grade solar cameras, and heavy investment in AI-powered analytics that it embeds directly into camera firmware. TP-Link Systems Inc. targets the residential and small business segment through its Tapo product line, leveraging existing brand recognition built through its networking hardware business to drive solar camera trial and cross-sell adoption. Fantasia Trading LLC, operating under the eufy brand, has established a strong presence in North America and Europe by emphasizing local storage, no-subscription pricing models, and integration with the broader eufy smart home ecosystem. Milesight competes on the strength of its IoT-grade hardware designed for demanding outdoor environments, offering solar cameras with dual-lens configurations, thermal imaging options, and open-platform ONVIF compatibility that appeals to system integrators. Swann, Toucan Solution,

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Solar-powered Security Camera Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $2.90B |

| Market Size (2033) | $8.40B |

| CAGR | 16.400% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Product, Connectivity, Distribution Channel, And Application |

| Companies Covered | TP-Link Systems Inc., Hangzhou Hikvision Digital Technology Co., Ltd., Maizic, Shenzhen LS VISION Technology Co., Ltd., Innotronik, Shenzhen LOYALTY-SECU Technology Co., LTD, Milesight, Fantasia Trading LLC (eufy), Toucan Solution, Swann |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Solar-powered Security Camera Market

You May Also Like

Specialist in Semiconductors and Electronics market intelligence.

Schedule Free Analyst Call