Scaffold-free 3D Cell Culture Market Overview & Analysis

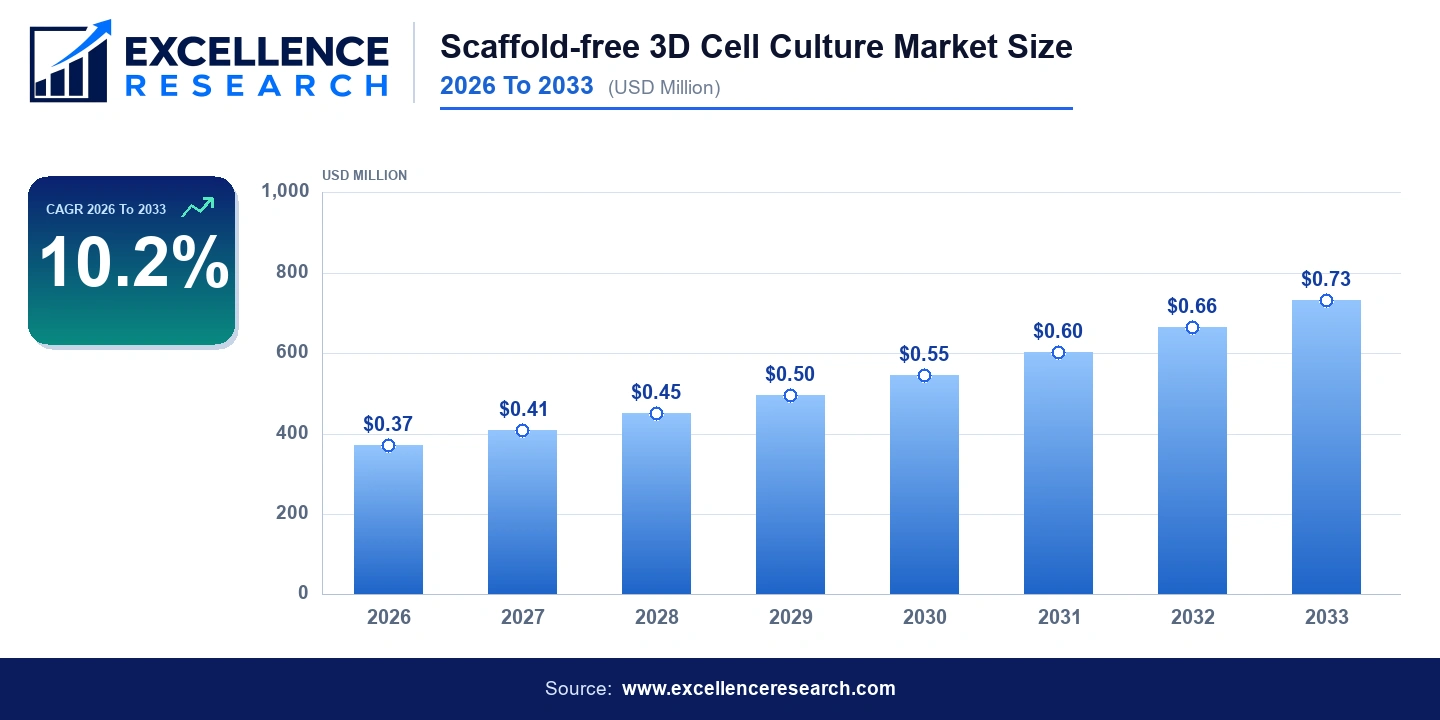

The Scaffold-free 3D Cell Culture Market size was valued at approximately USD 371 million in 2026 and is projected to reach USD 0.73 billion by 2033, expanding at a compound annual growth rate of 10.2% over the forecast period. This robust trajectory reflects accelerating adoption across pharmaceutical, biotechnology, and academic research sectors as scientists increasingly recognize that scaffold-free three-dimensional models replicate native tissue architecture far more accurately than conventional two-dimensional monolayer cultures. The Scaffold-free 3D Cell Culture Market share is distributed across a competitive field of specialized instrument manufacturers, consumables suppliers, and contract research organizations, with North America commanding the largest geographic portion in 2026 while Asia-Pacific registers the fastest regional growth. Spanning more than 45 countries, this market benefits from rising R&D expenditure in oncology, immuno-oncology, and regenerative medicine, all of which depend on physiologically relevant in vitro models to reduce costly late-stage clinical failures.

Key Report Takeaways

- By Technology: Spheroid Microplates with Ultra-Low Attachment (ULA) Coating held the largest technology share in 2026 due to their compatibility with standard liquid-handling automation, while Magnetic Levitation is the fastest-growing technology segment, advancing at double-digit rates as platforms from Nano3D Biosciences, Inc. gain traction in cardiac and neural research applications.

- By Application: Cancer Research accounted for the dominant application share in 2026, driven by demand for tumor spheroid models in immuno-oncology and precision oncology programs, while Stem Cell Research and Tissue Engineering is the fastest-growing application, underpinned by expanding regenerative medicine pipelines globally.

- By End Use: Biotechnology and Pharmaceutical Companies represented the largest end-use segment in 2026, reflecting high-volume consumable purchases by organizations such as Lonza Group AG and major integrated pharmaceutical firms, while Academic and Research Institutes are growing fastest as grant funding for three-dimensional biology expands across the United States, European Union, and China.

Market Drivers

The single most powerful driver of Scaffold-free 3D Cell Culture Market growth is the escalating failure rate of drug candidates that perform well in two-dimensional culture but collapse in clinical trials. The Tufts Center for the Study of Drug Development estimates that bringing a new drug to market costs more than USD 2.6 billion, and a significant portion of that expense stems from preclinical models that inadequately predict human tissue responses. Scaffold-free spheroid and organoid platforms dramatically improve predictive fidelity by preserving cell-cell junctions, hypoxic gradients, and extracellular matrix secretion patterns that are absent in flat cultures. Regulatory agencies including the U.S. Food and Drug Administration and the European Medicines Agency have begun issuing guidance encouraging the adoption of more physiologically relevant in vitro assays, further legitimizing and incentivizing the shift to three-dimensional systems documented in this Scaffold-free 3D Cell Culture Market report.

Secondary drivers include the global expansion of personalized medicine initiatives and increased funding for oncology research. The National Institutes of Health allocated over USD 7.5 billion to cancer research in fiscal year 2023, a portion of which directly supports development and validation of tumor spheroid models using platforms supplied by companies such as InSphero AG and Corning Incorporated. Simultaneously, the broad movement away from animal testing, codified in legislation such as the FDA Modernization Act 2.0 signed into law in late 2022, is prompting pharmaceutical and cosmetics companies alike to invest in scaffold-free three-dimensional alternatives. Scaffold-free 3D Cell Culture Market trends also show rising integration of these platforms with high-content imaging systems and artificial intelligence-driven data analysis, compressing assay cycle times and improving throughput without sacrificing biological relevance.

Segment Analysis

By Technology: Spheroid Microplates with ULA Coating represented approximately 48% of total market revenue in 2026, driven by the commercial success of products such as Corning's Ultra-Low Attachment microplates and Greiner Bio-One International GmbH's CELLSTAR ULA range. These products integrate seamlessly with standard robotic liquid-handling systems manufactured by Tecan Trading AG, enabling high-throughput screening at pharmaceutical companies that process tens of thousands of compound interactions annually. Hanging Drop Microplates, commercialized most prominently by InSphero AG through its GravityPLUS and GravityTRAP platforms, hold a meaningful secondary share, particularly in liver toxicity and metabolic disease research where precise spheroid sizing is critical. Magnetic Levitation, the technology championed by Nano3D Biosciences, Inc. using biocompatible magnetic nanoparticles, currently holds the smallest share but is projected to grow at the highest rate through 2033 as researchers demonstrate its utility in forming large, structurally complex tissue constructs for cardiac and neurological disease modeling.

By Application: Cancer Research dominated application-level demand in 2026, accounting for an estimated 42% of Scaffold-free 3D Cell Culture Market share. The rapid proliferation of immuno-oncology drug programs, including checkpoint inhibitor combinations and CAR-T cell therapies, requires three-dimensional tumor models that preserve immunosuppressive microenvironments. Drug Development and Toxicity Testing held the second-largest application share, with InSphero AG's 3D InSight Liver Microtissues and REPROCELL Inc.'s human tissue-derived assay systems directly addressing demand for predictive hepatotoxicity and cardiotoxicity testing. Stem Cell Research and Tissue Engineering, while currently third in revenue contribution, is projected to achieve the highest application-level CAGR through 2033 as regenerative medicine programs advance toward clinical translation and require scalable, scaffold-free expansion platforms for pluripotent stem cell-derived organoids.

By End Use: Biotechnology and Pharmaceutical Companies collectively account for the largest end-use revenue pool, with major consumers including contract development and manufacturing organizations like Lonza Group AG as well as large integrated pharmaceutical firms running internal discovery programs. These organizations purchase high volumes of ULA-coated microplates, proprietary hanging drop systems, and associated reagents from PromoCell GmbH and Merck KGaA. Academic and Research Institutes represent the second-largest end-use group and benefit from preferential pricing agreements negotiated through consortium purchasing programs in Europe and the United States. Hospitals form the smallest but an increasingly relevant end-use segment as translational research programs in precision oncology departments begin deploying patient-derived tumor spheroid assays to guide therapeutic decisions, a trend captured in the broader Scaffold-free 3D Cell Culture Market analysis compiled from clinical and commercial data across more than 45 countries.

Regional Analysis

North America dominates the Scaffold-free 3D Cell Culture Market with approximately 38% of global revenue in 2026, anchored by a dense concentration of pharmaceutical and biotechnology companies in the Boston-Cambridge corridor, San Francisco Bay Area, and Research Triangle Park. The presence of major market participants including Thermo Fisher Scientific Inc. and Corning Incorporated, combined with strong National Institutes of Health funding streams and a regulatory environment that actively encourages alternative testing methods through the FDA Modernization Act 2.0, sustains North American leadership. The United States alone accounts for the vast majority of this regional share, with Canada contributing meaningfully through government-backed regenerative medicine initiatives at institutions such as the Centre for Commercialization of Regenerative Medicine in Toronto.

Europe holds the second-largest regional position, contributing an estimated 31% of global Scaffold-free 3D Cell Culture Market share in 2026. Germany, Switzerland, and the United Kingdom are the principal national markets. Switzerland benefits from the headquarters presence of Lonza Group AG, Tecan Trading AG, and InSphero AG, creating a dense innovation cluster in the Basel and Zurich areas. Germany hosts Greiner Bio-One International GmbH's German operations and PromoCell GmbH, while Merck KGaA in Darmstadt supplies a broad portfolio of three-dimensional culture reagents and extracellular matrix products. European Union Horizon Europe funding, with over EUR 95 billion allocated across the 2021 to 2027 program, continues to channel resources into organ-on-chip and three-dimensional tissue engineering research that drives scaffold-free platform adoption.

Asia-Pacific is the fastest-growing region in the Scaffold-free 3D Cell Culture Market forecast period, with China, Japan, South Korea, and India collectively driving an above-average regional CAGR. China's 14th Five-Year Plan for Biotechnology has catalyzed domestic pharmaceutical R&D investment exceeding USD 30 billion annually, and Chinese academic institutions are rapidly adopting three-dimensional cell culture platforms for oncology and stem cell research. Japan is home to REPROCELL Inc., which specializes in human tissue-based assay systems, and benefits from a favorable regulatory posture toward regenerative medicine under the Act on the Safety of Regenerative Medicine. South Korea and India are emerging adopters, with contract research organizations in both countries adding scaffold-free three-dimensional capabilities to attract outsourced work from North American and European pharmaceutical sponsors.

Competitive Landscape

The competitive environment of the Scaffold-free 3D Cell Culture Market is moderately consolidated at the top, with Thermo Fisher Scientific Inc., Corning Incorporated, and Merck KGaA collectively commanding a substantial portion of consumables and instrument revenues. Thermo Fisher Scientific leverages its global distribution infrastructure and the Nunc brand portfolio to maintain broad reach across pharmaceutical, academic, and hospital end users. Corning Incorporated differentiates through material science expertise, offering proprietary surface chemistries in its ULA-coated product lines that competitors struggle to replicate. Merck KGaA competes across reagents, coatings, and three-dimensional culture media through its MilliporeSigma brand in North America. Lonza Group AG addresses the market primarily through its cell therapy manufacturing services, increasingly incorporating scaffold-free spheroid expansion steps into its commercial cell processing workflows. Mid-tier specialists such as InSphero AG, Greiner Bio-One International GmbH, and PromoCell GmbH compete on application-specific performance rather than breadth, targeting narrow but high-value niches in toxicity testing and primary cell culture. Nano3D Biosciences, Inc. and REPROCELL Inc. occupy technology-differentiated positions that insulate them from direct price competition in their respective magnetic levitation and human tissue ass

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Scaffold-free 3D Cell Culture Market |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $371M |

| Market Size (2033) | $732M |

| CAGR | 10.200% |

| Regions Covered | Global (45+ countries) |

| Segments Covered | Technology, Application, And End Use |

| Companies Covered | Thermo Fisher Scientific Inc., Merck KGaA, Corning Incorporated, Lonza Group AG, Greiner Bio‑One International GmbH, InSphero AG, REPROCELL Inc., Nano3D Biosciences, Inc., PromoCell GmbH, Tecan Trading AG |

Segmentation Covered

Key Companies Profiled (10)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Scaffold-free 3D Cell Culture Market

You May Also Like

Specialist in Biotechnology market intelligence.

Schedule Free Analyst Call