Silicon Carbide Power Semiconductor Market Overview & Analysis

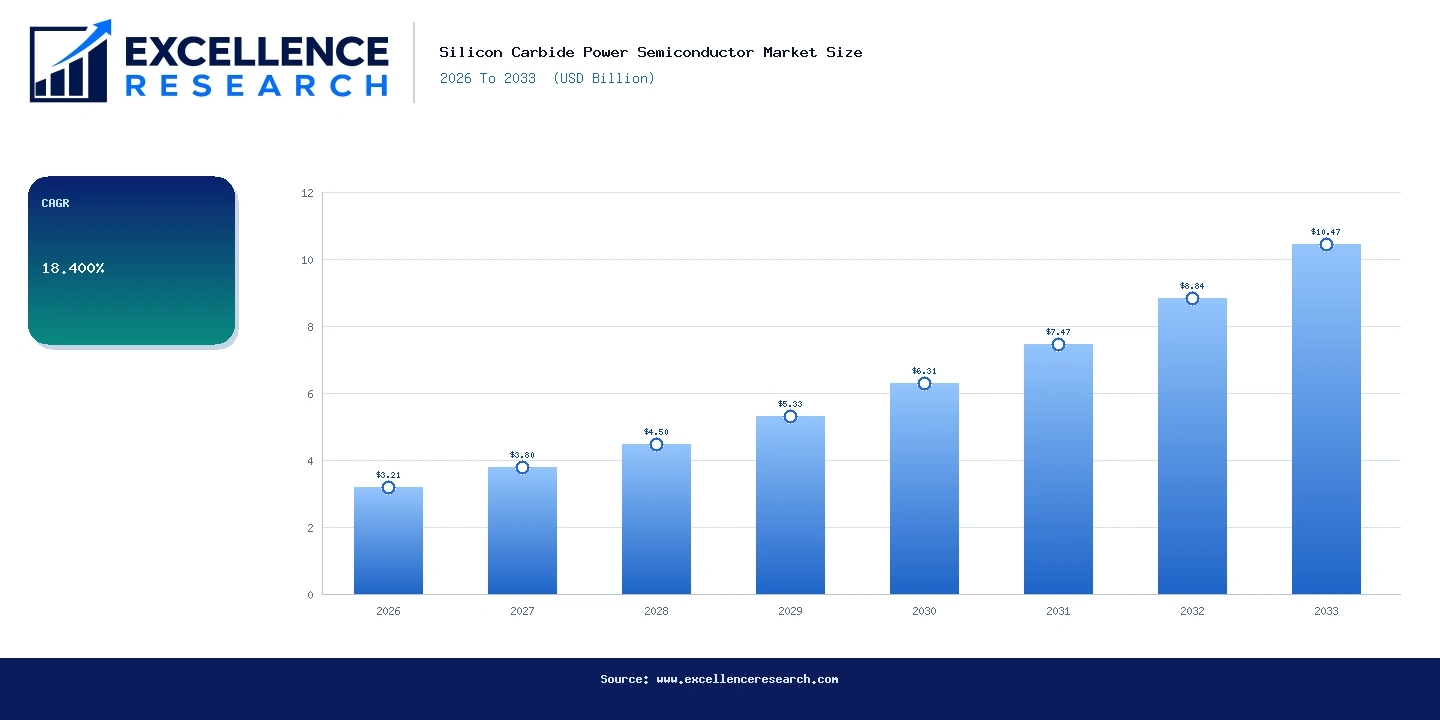

The global silicon carbide (SiC) power semiconductor market is entering its most consequential growth phase since the technology's commercial inception in the mid-1990s. Three structural forces are colliding simultaneously: the rapid scaling of electric vehicle (EV) platforms that demand higher inverter efficiency, the accelerating rollout of utility-scale solar and wind installations requiring grid-tie inverters, and a generational shift in industrial motor drives toward energy efficiency mandates. Each of these end-markets is placing SiC at the center of its power conversion architecture, and the resulting demand pull is unlike anything the semiconductor industry has seen for a materials transition in over two decades. The market was valued at USD 3.21 billion in 2026. Excellence Research projects it will reach USD 10.47 billion by 2033, expanding at a compound annual growth rate of 18.4% over the forecast period. This is not a linear growth story. The 2026 to 2028 window will see the most intense supply-demand imbalance, driven by EV OEM production ramps at Tesla, BYD, Volkswagen Group, and Stellantis, all of whom have qualified SiC MOSFETs and diodes as primary switching devices in their next-generation 800V onboard chargers and traction inverters. Post-2028, incremental capacity from Wolfspeed's Siler City, North Carolina facility and STMicroelectronics' Catania substrate expansion will begin to alleviate structural shortfalls. EV traction inverters represent the single largest application segment, accounting for 38.7% of total SiC revenue in 2026. A standard 150 kW EV traction inverter requires 24 to 48 SiC MOSFETs depending on the switching topology; at USD 3.80 to USD 6.20 per die, the bill of materials cost per vehicle for SiC alone ranges from USD 91 to USD 298. This content-per-vehicle figure is roughly 3.4 times higher than equivalent silicon IGBT solutions, but the efficiency gain of 1.5 to 3 percentage points in inverter efficiency translates to meaningful range extension or battery cost reduction at the vehicle level. This value proposition has proven sufficient to overcome procurement team resistance and is driving rapid design-win momentum. Asia Pacific dominates global SiC consumption at 52% in 2026, led by China's EV production ecosystem where BYD alone manufactured 3.02 million battery-electric and plug-in hybrid vehicles in 2025. China's domestic SiC substrate supply chain remains underdeveloped relative to its consumption needs, creating a significant import dependency on Japanese (Showa Denko, SICC), European (Wolfspeed, SiCrystal), and American suppliers. The Chinese government's 14th Five-Year Plan explicitly targets self-sufficiency in third-generation semiconductors by 2030, with over CNY 28 billion committed to SiC and GaN supply chain development through state investment funds and provincial subsidies. The competitive landscape is consolidating around a small number of vertically integrated suppliers. Wolfspeed leads in substrate capacity; STMicroelectronics holds the strongest automotive design-win position with over 85 vehicle platform qualifications by end-2025; Infineon Technologies AG has the broadest industrial and renewable energy customer base; and ROHM Semiconductor is gaining share in Japanese OEM EV programs. ON Semiconductor completed its acquisition of GTAT's SiC boule growth assets in 2024, strengthening its substrate independence. New entrants including Sanan IC, SICC, and TanKeBlue (all China-based) are scaling aggressively but face a 3 to 5 year qualification lag for tier-1 automotive programs. Key restraints include the capital intensity of SiC substrate production (a single 150mm SiC boule growth furnace costs USD 2.2 to USD 3.8 million versus USD 0.6 million for equivalent silicon equipment), chronic micropipe defect density challenges that reduce die yield, and the 18 to 36 month automotive qualification cycle that creates lead-time risk for OEM supply planners. Despite these constraints, the long-term trajectory is firmly upward: every major OEM, industrial drive manufacturer, and renewable energy inverter supplier is in active SiC qualification. The transition from silicon to SiC is not a question of if, but of how fast supply can scale to meet demand.

Key Research Takeaways

Report Scope & Coverage

| Attribute | Details |

|---|---|

| Report Title | Silicon Carbide Power Semiconductor Market Size, Share, Trends & Forecast 2026 To 2033 |

| Base Year | 2026 |

| Historical Period | 2021 To 2025 |

| Forecast Period | 2026 To 2033 |

| Market Size (2026) | $3.21B |

| Market Size (2033) | $10.47B |

| CAGR | 18.400% |

| Regions Covered | Global (55+ countries) |

| Segments Covered | Product Type, Voltage Rating, Application, And Region |

| Companies Covered | Wolfspeed Inc., STMicroelectronics N.V., Infineon Technologies AG, onsemi (ON Semiconductor), ROHM Semiconductor, Mitsubishi Electric Corp., Sanan Integrated Circuit (Sanan IC), SICC Co., Ltd., Vishay Intertechnology, General Electric (GE Power), TanKeBlue Semiconductor, Showa Denko K.K. and others |

Segmentation Covered

Key Companies Profiled (15)

Full profiles include company overview, product portfolio, revenue, SWOT analysis, recent developments, and strategic initiatives.

Related Press Releases & News

Frequently Asked Questions — Silicon Carbide Power Semiconductor Market

You May Also Like

11 years covering wide-bandgap semiconductor markets, EV power systems, and industrial power conversion. Previously with IHS Markit Power & Energy team.

Schedule Free Analyst Call